Serious writing for

serious readers

This short simple book is the best possible introductory guide to thinking about your personal finances.

Summary

9 October 2021

I came across the blog “Of Dollars and Data” written by Nick Maggiulli after seeing it in either a magazine or an online article, but cannot be more specific.

I immediately subscribed to the blog. (I manage all my blog subscriptions using the RSS reader that is built into Microsoft Outlook.) You can also subscribe simply by providing your email into the subscription box on the blog.

The blog is free to read and I recommend it.

I was very struck by the 8 September 2020 post “What Your Psychology Says About Your Relationship with Money.” Reviewing my Amazon account just now, I see that I purchased this book, which the article praises highly, that very same day.

I often buy books and then let a long time lapse before I read them. My current career record is 50 years! However, on 12 September 2020 I received a WhatsApp message from my son-in-law about the book saying that he was reading it. He is developing an interest in investment and also subscribed to the blog based upon my recommendation.

That gave me the small encouragement I needed to move the book nearer to the top of my reading pile and I read it a few weeks later. It is very easy to read.

The blurb on the back cover states the following:

“Morgan Housel is a partner at the Collaborative Fund.

Previously he was a columnist at “The Wall Street Journal” and “The Motley Fool.”

He is a two-time winner of the Best in Business Award from the Society of American Business Editors and Writers, the New York Times Sydney Award, and a two-time finalist for the Gerald Loeb Award for Distinguished Business Writing.”

Advertisement

Click image

Including the endnotes and acknowledgements the book is only 242 pages. Furthermore, it is a reasonable size font, and well spaced, so very easy to read.

It has 20 chapters, each with a subtitle which I have reproduced immediately after the chapter title, separated by a colon.

“Introduction: The Greatest Show on Earth

- No One’s Crazy: Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works.

- Luck & Risk: Nothing is as good or as bad as it seems.

- Never Enough: When rich people do crazy things.

- Confounding Compounding: $81.5 billion of Warren Buffett’s $84.5 billion net worth came after his 65th birthday. Our minds are not built to handle such absurdities.

- Getting Wealthy vs. Staying Wealthy: Good investing is not necessarily about making good decisions. It’s about consistently not screwing up.

- Tails, You Win: You can be wrong half the time and still make a fortune.

- Freedom: Controlling your time is the highest dividend money pays.

- Man in the Car Paradox: No one is impressed with your possessions as much as you are.

- Wealth Is What You Don’t See: Spending money to show people how much money you have is the fastest way to have less money.

- Save Money: The only factor you can control generates one of the only things that matters. How wonderful.

- Reasonable > Rational: Aiming to be the most reasonable works better than trying to be coldly rational.

- Surprise!: History is the study of change, ironically used as a map of the future.

- Room for Error: The most important part of every plan is planning on your plan not going according to plan.

- You’ll Change: Long-term planning is harder than it seems because people’s goals and desires change over time.

- Nothing’s Free: Everything has a price, but not all prices appear on labels.

- You & Me: Beware taking financial cues from people playing a different game than you are.

- The Seduction of Pessimism: Optimism sounds like a sales pitch. Pessimism sounds like someone trying to help you.

- When You’ll Believe Anything: Appealing fictions, and why stories are more powerful than statistics.

- All Together Now: What we’ve learned about the psychology of your own money.

- Confessions: The psychology of my own money.

Postscript: A Brief History of Why the US Consumer Thinks the Way They Do

Endnotes

Acknowledgements”

Below I have shared two short extracts which particularly struck me. They will let you appreciate the author's writing style.

The author compares two very different people. The first one made lots of money.

“I spent my college years working as a valet at a nice hotel in Los Angeles.

One frequent guest was a technology executive. He was a genius, having designed and patented a key component in Wi-Fi routers in his 20s. He had started and sold several companies. He was wildly successful.

He also had a relationship with money I described as a mix of insecurity and childish stupidity.

He carried a stack of hundred dollar bills several inches thick. He showed it to everyone who wanted to see it and many who didn’t. He bragged openly and loudly about his wealth, often while drunk and always apropos of nothing.

One day he handed one of my colleagues several thousand dollars of cash and said, “go to the jewellery store down the street and get me a few $1,000 gold coins.”

An hour later, gold coins in hand, the tech executive and his buddies gathered around by a dock overlooking the Pacific Ocean. They then proceeded to throw the coins into the sea, skimming them like rocks, cackling as they argued whose went furthest. Just for fun.

Days later he shattered a lamp in the hotel’s restaurant. A manager told him it was a $500 lamp and he’d have to replace it.

“You want five hundred dollars?” the executive asked incredulously, while pulling a brick of cash from his pocket and handing it to the manager. “Here’s five thousand dollars. Now get out of my face. And don’t ever insult me like that again.”

You may wonder how long this behaviour could last, and the answer was “not long.” I learned years later that he went broke.”

The author reminds us of his key message.

“The premise of this book is that doing well with money as a little to do with how smart you are and a lot to do with how you behave. And behaviour is hard to teach, even to really smart people.”

He then tells us about a person who was the opposite of the above tech entrepreneur.

“A genius who loses control of their emotions can be a financial disaster. The opposite is also true. Ordinary folks with no financial education can be wealthy if they have a handful of behavioural skills that have nothing to do with formal measures of intelligence.

My favourite Wikipedia entry begins: “Ronald James Read was an American philanthropist, investor, janitor, and gas station attendant.”

Ronald Read was born in rural Vermont. He was the first person in his family to graduate high school, made all the more impressive by the fact that he hitchhiked to campus each day.

For those who knew Ronald Read, there wasn’t much else worth mentioning. His life was about as low-key as they come.

Read fixed cars at a gas station for 25 years and swept floors at JCPenney for 17 years. He bought a two-bedroom house for $12,000 at age 38 and lived there for the rest of his life. He was widowed at age 50 and never remarried. A friend recalled that his main hobby was chopping firewood.

Read died in 2014, age 92. Which is when the humble rural janitor made international headlines.

2,813,503 Americans died in 2014. Fewer than 4,000 of them had a net worth of over $8 million when they passed away. Ronald Read was one of them.

In his will the former janitor left $2 million to his stepkids and more than $6 million to his local hospital and library.

Those who knew Read were baffled. Where did he get all that money?

It turned out there was no secret. There was no lottery win and no inheritance. Read save what little he could and invested it in blue-chip stocks. Then he waited, for decades on end, as tiny savings compounded into more than $8 million.

That’s it. From janitor to philanthropist.”

The author then contrasts Read with a very successful finance professional.

“A few months before Ronald Read died, another man named Richard was in the news.

Richard Fuscone was everything Ronald Read was not. A Harvard-educated Merrill Lynch executive with an MBA, Fuscone had such a successful career in finance that he retired in his 40s to become a philanthropist. Former Merrill CEO David Komansky praised Fuscone’s “business savvy, leadership skills, sound judgement and personal integrity.” Crain’s business magazine once included him in a “40 under 40” list of successful businesspeople.

But then – like the gold-coin-skipping tech executive – everything fell apart.

In the mid-2000’s Fuscone borrowed heavily to expand an 18,000-square foot home in Greenwich, Connecticut that had 11 bathrooms, two elevators, two pools, seven garages, and cost more than $90,000 a month to maintain.

Then the 2008 financial crisis hit.

The crisis occurred virtually everyone’s finances. It apparently turned to Fuscone’s into dust. High debt and illiquid assets left him bankrupt. “I currently have no income,” he allegedly told a bankruptcy judge in 2008.

First his Palm Beach house was foreclosed.

In 2014 it was the Greenwich mansion’s turn.

Five months before Ronald Read left his fortune to charity, Richard Fuscone’s home – where guests recalled the “thrill of dining and dancing atop a see-through covering on the home’s indoor swimming pool” – was sold in a foreclosure auction for 75% less than an insurance company figured it was worth.

Ronald Read was patient; Richard Fuscone was greedy. That’s all it took to eclipse the massive education and experience gap between the two.”

The stories of Ronald Read and Richard Fuscone contain a very powerful message about finance, and what makes it very different from other areas of human activity.

“The lesson here is not to be more like Ronald and less like Richard – though that’s not bad advice.

The fascinating thing about these stories is how unique they are to finance.

In what other industry does someone with no college degree, no training, no background, no formal experience, and no connections massively outperform someone with the best education, the best training, and the best connections?

I struggle to think of any.

It is impossible to think of a story about Ronald Read performing a heart transplant better than a Harvard-trained surgeon. Or designing a skyscraper superior to the best-trained architects. There will never be a story of a janitor outperforming the world’s top nuclear engineers.

But these stories do happen in investing.

The fact that Ronald Read can coexist with Richard Fuscone has two [possible] explanations:

- Financial outcomes are driven by luck, independent of intelligence and effort. That’s true to some extent, and this book will discuss it in further detail. Or,

- (and I think more common), that financial success is not a hard science. It’s a soft skill, where how you behave is more important than what you know.

I call this soft skill the psychology of money. The aim of this book is to use short stories to convince you that soft skills are more important than the technical side of money. I’ll do this in a way that will help everyone – from Read to Fuscone and everyone in between – make better financial decisions.”

The message below particularly resonates with me. The reason is that I regularly tell people not to invest in shares if they cannot stand watching their investments go down in value.

“Every job looks easy when you’re not the one doing it because the challenges faced by someone in the arena are often invisible to those in the crowd.

…

Most things are harder in practice than they are in theory. Sometimes this is because we’re overconfident. More often it’s because we’re not good at identifying what the price of success is, which prevents us from being able to pay it.The S&P 500 increased 119-fold in the 50 years ending 2018. All you had to do was sit back and let your money compound. But, of course, successful investing looks easy when you’re not the one doing it.

“Hold stocks for the long run,” you’ll hear. It’s good advice.

But do you know how hard it is to maintain a long-term outlook when stocks are collapsing?

Like everything else worthwhile, successful investing demands a price. But its currency is not dollars and cents. It’s volatility, fear, doubt, uncertainty, and regret – all of which are easy to overlook until you’re dealing with them in real time.

The inability to recognise that investing has a price can tempt us to try to get something for nothing. Which, like shoplifting, rarely ends well.

So you want a new car. It costs $30,000. You have three options:

- Pay $30,000 for it,

- find a cheap are used one, or

- steal it.

In this case, 99% of people know to avoid the third option, because the consequences of stealing a car outweigh the upside.

Let’s say you want to earn an 11% annual return over the next 30 years so you can retire in peace. Does this reward come free? Of course not. The world is never that nice. There’s a price tag, a bill that must be paid.

In this case it’s a never-ending taunt from the market, which gives big returns and takes them away just as fast.

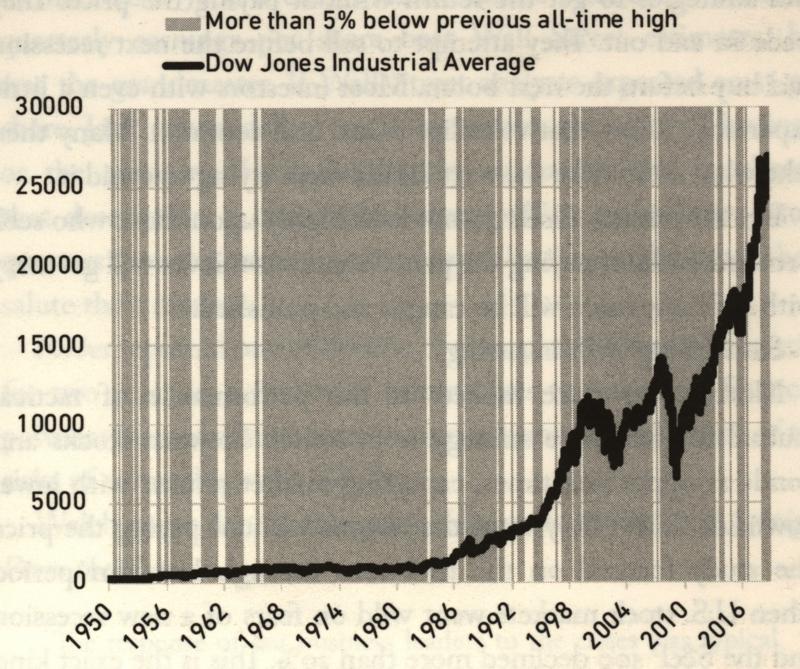

Including dividends the Dow Jones Industrial Average returned about 11% per year from 1950 to 2019, which is great. But the price of success during this period was dreadfully high.

The shaded lines in the chart show when it was at least 5% below its previous all-time high.

This is the price of market returns. The fee. It is the cost of admission. And it hurts.

Like most products, the bigger the returns, the higher the price.

Netflix stock returned more than 35,000% from 2002 to 2018, but traded below its previous all-time high on 94% of days. Monster Beverage returned 319,000% from 1995 to 2018 – among the highest returns in history – but traded below its previous high 95% of the time during that period.

Now here’s the important part. Like the car, you have a few options: You can pay this price, accepting volatility and upheaval. Or you can find an asset with less uncertainty and a lower payoff, the equivalent of a used car. Or you can attempt the equivalent of grand-theft auto: Try to get the return while avoiding the volatility that comes along with it.

Many people in investing choose the third option. Like a car thief – though well-meaning and law-abiding – they form tricks and strategies to get the return without paying the price. They trade in and out. They attempt to sell before the next recession and buy before the next boom. Most investors with even a little experience know that volatility is real and common. Many then take what seems like the next logical step: trying to avoid it.

But the Money Gods do not look highly upon those who seek a reward without paying the price. Some car thieves will get away with it. Many more will be caught and punished.

Same with investing.

Morningstar once looked at the performance of tactical mutual funds, whose strategy is to switch between stocks and bonds at opportune times, capturing market returns with lower downside risk. They want the returns without paying the price. The study focused on the mid-2010 through late 2011 period, when US stock markets went wild on fears of a new recession and the S&P 500 declined more than 20%. This is the exact kind of environment the tactical funds are supposed to work in. It was their moment to shine.

There were, by Morningstar’s count, 112 tactical mutual funds during this period. Only nine had better risk-adjusted returns than a simple 60/40 stock-bond fund. Less than a quarter of the tactical funds had smaller maximum drawdowns than the leave-it-alone index. Morningstar wrote: “With A few exceptions, [tactical funds] gained less, were more volatile, or were subject to just as much downside risk” as the hands-off fund.

Individual investors fall for this when making their own investments, too. The average equity fund investor underperformed the funds they invested in by half a percent per year, according to Morningstar – the result of buying and selling when they should have just bought and held.

The irony is that by trying to avoid the price, investors end up paying double.

…

The question is: Why do so many people who are willing to pay the price of cars, houses, food, and vacations try so hard to avoid paying the price of good investment returns?The answer is simple: The price of investing success is not immediately obvious. It’s not a price tag you can see, so when the bill comes due it doesn’t feel like a fee for getting something good. It feels like a fine for doing something wrong. And while people are generally fine with paying fees, fines are supposed to be avoided. You’re supposed to make decisions that pre-empt and avoid fines. Traffic fines and IRS fines mean you did something wrong and deserve to be punished. The natural response for anyone who watches their wealth decline and views that drop as a fine is to avoid future fines.

It sounds trivial, but thinking of market volatility as a fee rather than a fine is an important part of developing the kind of mindset that lets you stick around long enough for investing gains to work in your favour.

Few investors have the disposition to say, “I’m actually fine if I lose 20% of my money.” This is doubly true for new investors who have never experienced a 20% decline.

But if you view volatility as a fee, things look different.

Disneyland tickets cost $100. But you get an awesome day with your kids you’ll never forget. Last year more than 18 million people thought that fee was worth paying. Few felt the hundred dollars was a punishment or a fine. The worthwhile trade-off of fees is obvious when it’s clear you’re paying one.

Same with investing, where volatility is almost always a fee, not a fine.

Market returns are never free and never will be. They demand you pay a price, like any other product. You’re not forced to pay this fee, just like you’re not forced to go to Disneyland. You can go to the local county fair where tickets might be $10, or stay home for free. You might still have a good time. But you’ll usually get what you pay for. Same with markets. The volatility/uncertainty fee – the price of returns – is the cost of admission to get returns greater than low-fee parks like cash and bonds.

The trick is convincing yourself that the market’s fee is worth it. That’s the only way to properly deal with volatility and uncertainty – not just putting up with it, but realising that it’s an admission fee worth paying.

There’s no guarantee that it will be. Sometimes it rains at Disneyland. But if you view the admission fee as a fine, you’ll never enjoy the magic.

Find the price, then pay it.

I have seen my investment portfolio fall by over 20% on several occasions:

I found losing large amounts of money as painful and unpleasant as anyone else would. However I did not panic, I did not sell anything just because it had fallen, and I continued my normal investing policies. That is what living with volatility requires.

Your ability to earn a high income primarily depends upon your skills and abilities. That is true regardless of whether your skill is playing football or giving tax advice.

Your ability to retain some of your income and become rich depends almost entirely on the way that you think about money. Your personal psychology of money.

Understanding that comes before everything, and in particular long before you become a serious investor. It matters from the time you get your first job.

Apart from some of the historical facts and stories contained in the book, and some of the data, I cannot think of anything major that I personally learned from the book.

The reason is that I imbibed some of these messages from my parents who were very poor but careful with how they managed their money. (I did not adopt all my parents' attitudes and beliefs. One bad equity investment had put my father off shares for life. My mother was too pessimistic.)

The rest of the principles I figured out for myself as I went through life.

Growing up very poor encourages you not to waste money. Even as a PricewaterhouseCoopers partner, my wristwatch was a Timex digital watch that had cost me about £20! In the last few years of my career, I was saving more than 50% of my income.

I rate this book so highly that I am putting it first in my recommended list of investing books. Everyone should read it as soon as they start work.

The further you are into your financial life, the more important the book will be to you unless you have already learned all of these lessons through your own personal experience.

Even if you think you know it all already, reading this book will be a quick and extremely valuable health check of your personal psychology of money.

Follow @Mohammed_Amin