Serious writing for

serious readers

Summary

1 October 2009

This article is based upon a talk I gave in July 2009 in London for the Institute of Islamic Banking and Insurance.

The year 2008 saw the most severe crisis in the global financial system since the great depression of the 1930s. At conferences on Islamic finance one question occurs repeatedly: "Would it have happened with Islamic finance?"

To address this question systematically, one needs to consider the following:

These are complex issues and this short article can only provide signposts for further study.

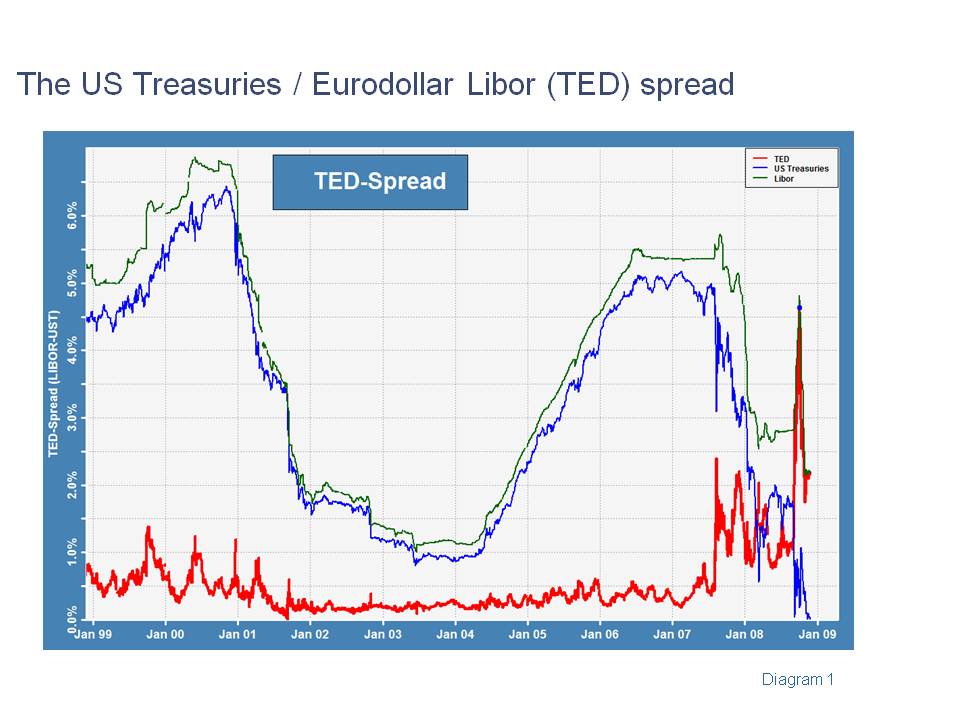

Diagram 1 shows the difference between Eurodollar LIBOR (the London Interbank Offered Rate at which prime banks lend to each other) and the yield on US Treasury securities. As the US government can print dollars and has never defaulted, its dollar-denominated liabilities are regarded as risk free, so LIBOR always exceeds the Treasuries’ yield. The spread between them (the TED spread) has typically been under 1%, and for most of the last decade was under 0.5%. However it spiked upwards in mid-2007 to nearly 2.5%, remained volatile and in late 2008 soared to over 4.5%. What was happening?

Newspapers report that in mid-2007 the UK bank Northern Rock became unable to fund its operations in the interbank money market. Liquidity had disappeared, evidenced by the almost instantaneous rise in the TED spread to levels unprecedented in recent memory. The historical phrase "credit crunch" reappeared; an environment where even credit worthy borrowers are simply unable to access funds. In the UK, the USA and elsewhere, central banks had to supply huge amount of liquidity to the interbank money market, but with limited impact as can be seen from the TED spread chart. In September 2008 Lehman Brothers collapsed in the largest bankruptcy ever by size of assets.

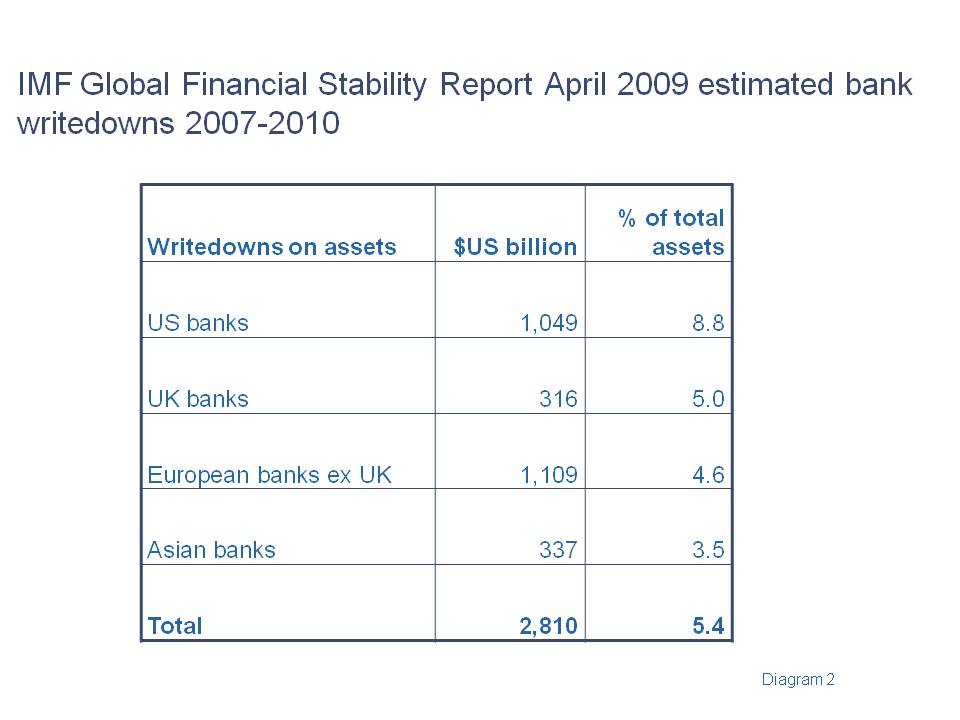

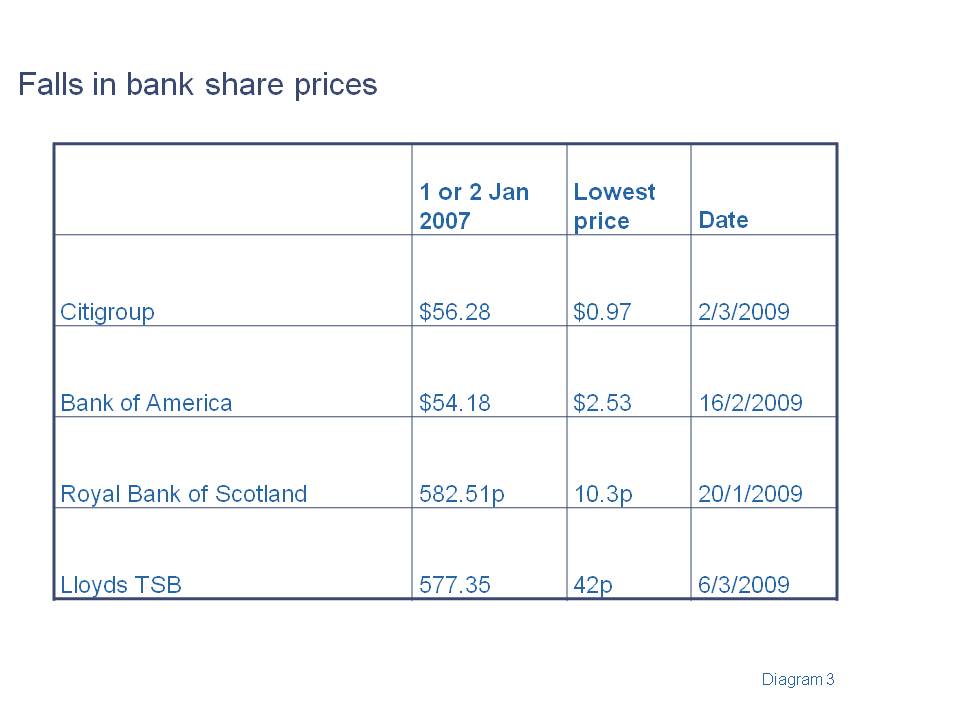

Diagram 2 shows the International Monetary Fund's projections for the period 2007 - 2010 of write-downs on assets by banks by region. The US write-down of 8.8% of total assets is enough to approximately wipe out almost all the capital of the US banking system. It is therefore no surprise to see the massive falls in bank share prices illustrated on Diagram 3.

Governments have been forced to support their banking sectors with capital injections. Otherwise their economies faced a perpetual downward spiral: losses reducing banks’ capital, making them less willing to lend, leading to customer bankruptcies resulting in more bank losses.

A number of different factors came together in what has been called "a perfect storm."

This is a mortgage loan to a borrower with flaws in his or her credit rating, such as a previous bankruptcy. Normally such borrowers need additional collateral for loans and face higher interest rates.

However, several years of strongly rising house prices caused lenders to relax their lending criteria. Loan to value ratios rose towards 100% and low starter interest rates were introduced (typically for the first two years of the mortgage) to be recouped by higher interest rates for the remaining 28 years of the typical 30 year US mortgage. In many cases the borrowers knew that they could not afford the monthly payments after the initial two-year low interest period expired; they were relying on rising house prices to enable a profit on sale or refinancing.

However US house prices started to fall. Faced with negative equity many US householders simply walked away from their properties. Unlike the UK, in many US states residential mortgages are non-recourse, with no personal liability for the borrower. The mortgage default rates on these sub-prime mortgages were much higher than predicted by the lenders’ credit models; however those models were based upon the historical behaviour of prime borrowers, not sub-prime borrowers who behaved differently.

Over the years, the US mortgage market had moved away from a "lend and collect" model (the bank lends on a mortgage and collect it back over 30 years) to an "originate to sell" model (the bank makes a mortgage loan in order to sell it on.) Originating loans and selling them on means that banks make profits from lending as much as possible, provided that the loans can be sold on; once the loan has been sold the bank is relatively indifferent to its collectibility.

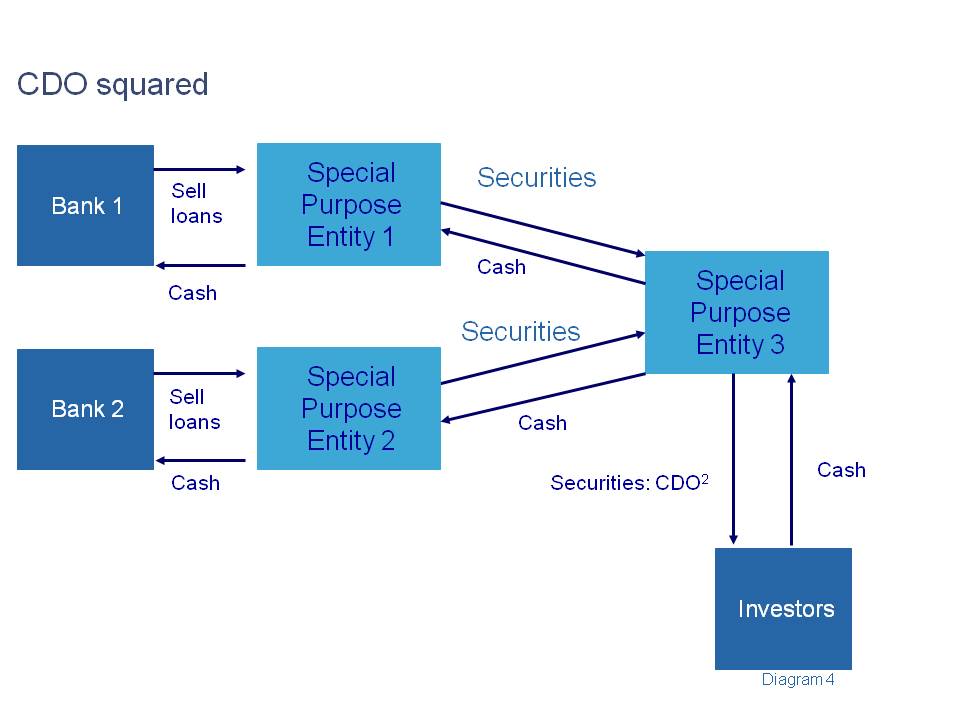

As well as securitising original loans, investment bankers developed more complex structures such as CDO2 (collateralised debt obligations squared) illustrated on Diagram 4.

Here CDO securities created by Bank 1 and Bank 2 selling their customer loans are purchased by Special Purpose Entity (SPE) 3 which pays for them by issuing CDO securities to investors. As these are CDOs based on other CDOs, they are called CDO2.

The challenge with such complex structures is that it becomes almost impossible to accurately project likely defaults on the original customer loans to the likely defaults on the securities issued by SPE 3. In many cases, complex CDO structures involved some sub-prime mortgages being blended with prime mortgages to boost the yield of the overall package of assets. Accordingly, once defaults started happening in the relatively small sub-prime market, that led to a collapse in the market value of a much larger amount of CDOs.

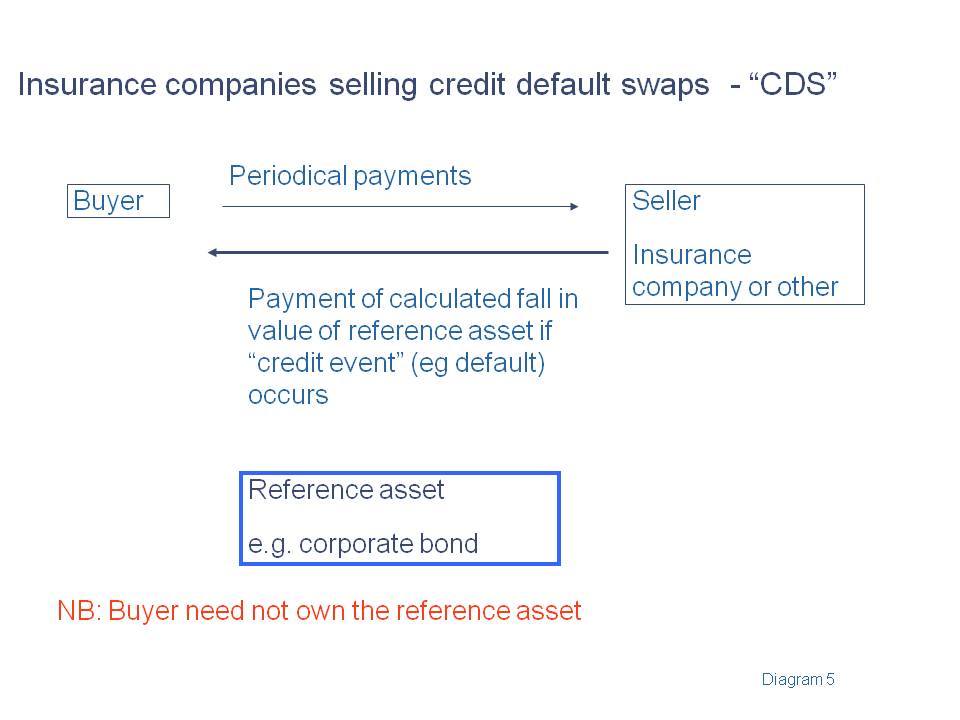

Under a credit default swap contract (CDS) as shown on Diagram 5, the seller is paid a regular amount each year by the buyer of the CDS. If a credit event occurs in relation to the underlying asset which is referenced by the CDS, the seller pays the buyer for the fall in value of the reference asset. However, the buyer does not need to own the reference asset; in that case the CDS buyer is simply speculating that the reference asset will fall into default.

Until a credit event occurs, the seller of the CDS receives cash each year. Accordingly, to assess its profits, it needs to assess an actuarial liability for the likelihood of paying out under the CDS. If it underestimates the CDS payout risk, it will erroneously report profits each year. Some very large CDS sellers did report large profits, only to find that as credit market conditions changed they faced losses on their CDS contracts large enough to bankrupt them. Accordingly the US government had to inject capital into the largest US insurance company, American International Group, to save it from bankruptcy.

The existence of CDS contracts also changes the incentives that apply in the capital markets. A CDS purchaser may be in a position to directly influence the solvency of the underlying borrower of the reference asset. E.g. the CDS may be over bonds issued by a bank. If the CDS buyer can force the borrowing bank into distress, for example by forcing down its share price by short selling its shares (which can lead to counterparties becoming reluctant to deal with it) the buyer will make profits from the resulting default due to its ownership of the CDS contracts.

The economies of the UK and USA had not suffered a serious recession for many years. In these benign business conditions, companies had gradually increased their gearing, as interest on debt is tax deductible whereas dividends on share capital are not tax deductible. The high gearing was particularly striking in companies owned by private equity firms, which were typically very highly leveraged. If economic conditions worsened, such firms would risk insolvency.

All of the above factors came together in the crisis.

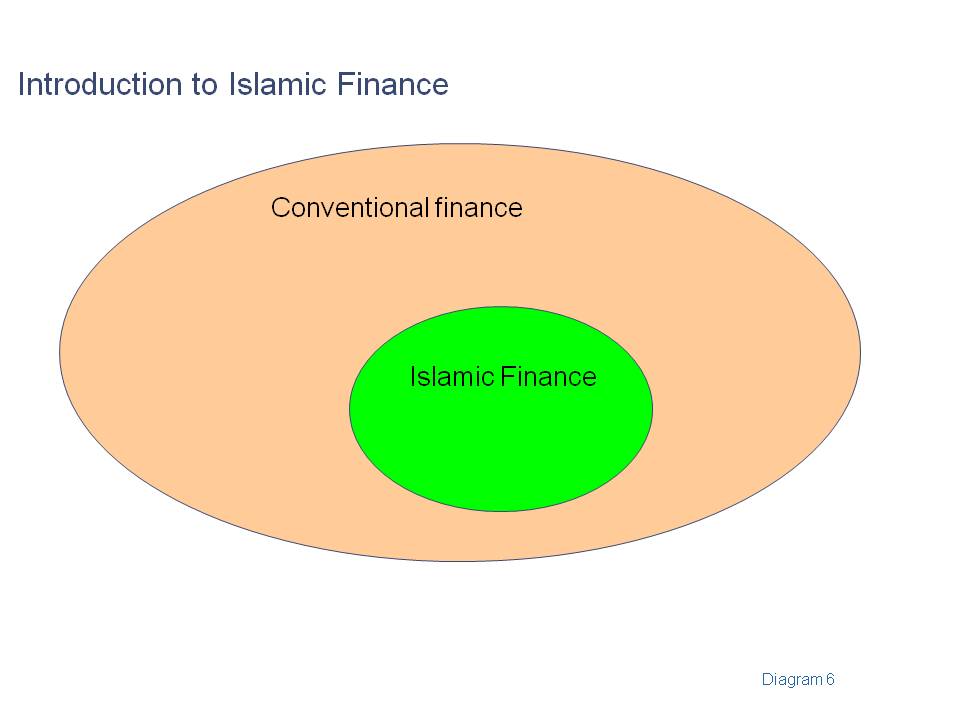

As illustrated on Diagram 6, Islamic finance is a strict subset of conventional finance. Everything done in Islamic finance can be done using conventional contracts; the conventional contracting parties need not care whether their contracts are Shariah compliant. Conversely, there are many contracts used in conventional finance which cannot be used in Islamic finance. Most practitioners consider that Islamic finance prohibits:

Some of the contracts used in Islamic finance have similar economic characteristics to conventional contracts. For example, the customer in a murabaha contract or an ijara contract makes predetermined cash payments, which can be identical in amount and timing to those a conventional customer might pay under an interest-bearing loan or under a conventional leasing contract.

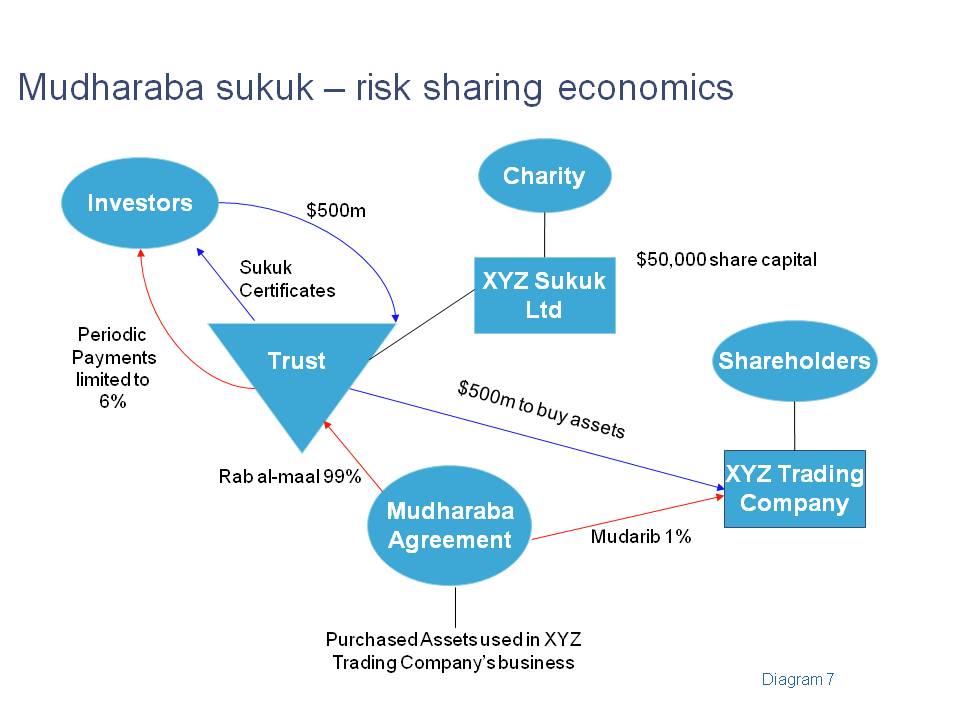

However, other contracts used in Islamic finance have economic characteristics which differ from the contracts commonly used in conventional finance. For example, in a mudharaba contract, losses are born exclusively by the rab al maal (the capital provider) and not by the mudarib (the entrepreneur or business manager.) Diagram 7 shows a sukuk structure where the originator, XYZ Trading Company, does not make any payment to the sukuk investors (directly or indirectly) if the business being conducted with the funds raised fails to generate sufficient profits. This is quite different from a conventional bond.

There are three main reasons why Islamic finance would have been less likely to result in the global financial crisis.

Certain contracts are simply prohibited in Islamic finance. The prohibition of gharar and of selling things not owned precludes complex contracts such as CDO2 and CDS. Accordingly many of the contracts that have led to the greatest difficulties would never have been used.

The Islamic financial system distributes risk differently from conventional finance. While the same aggregate business losses may arise, their different distribution makes the system less likely to "seize up" or result in corporate bankruptcies.

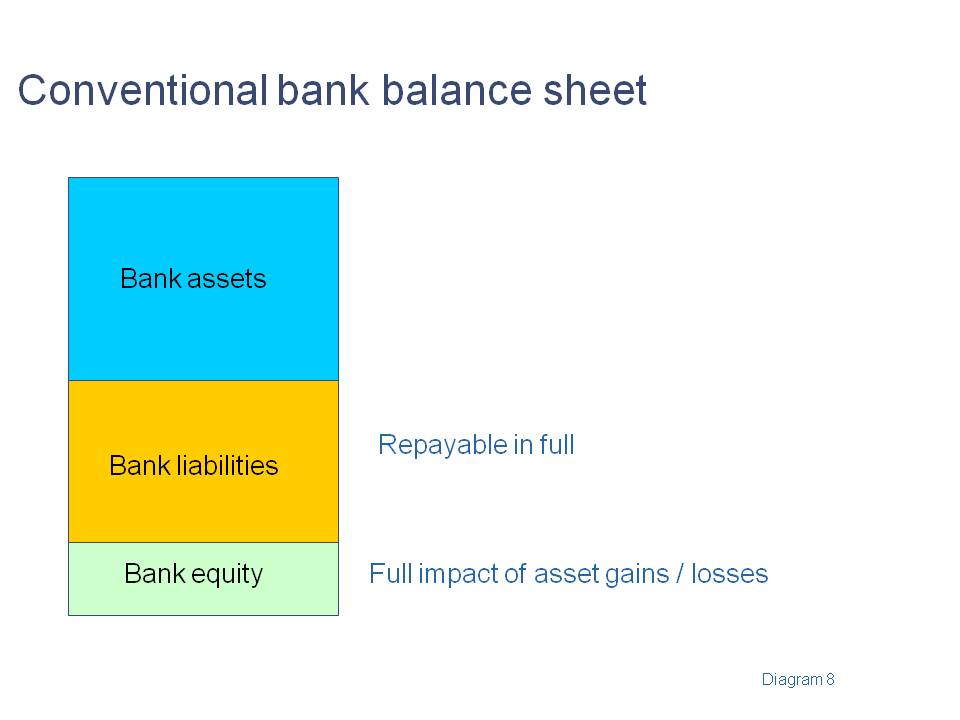

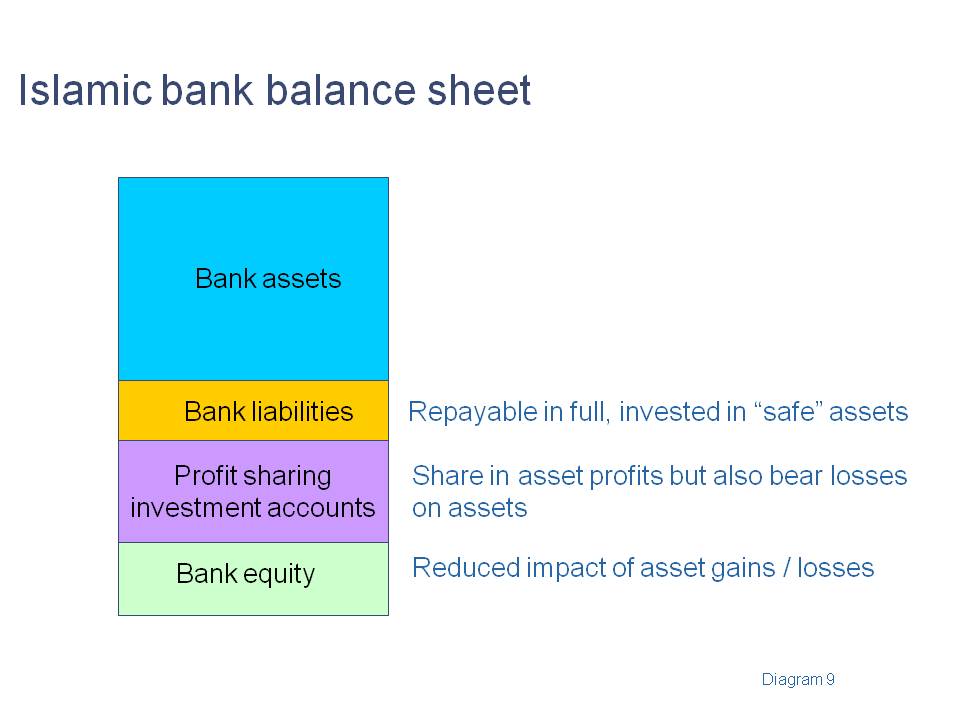

For example, with a conventional bank, as in Diagram 8, liabilities are repayable in full so losses fall exclusively on the banks equity.

Accordingly, even a relatively small asset default rate can seriously impair the banks equity and its ability to lend. Conversely, the Islamic bank on Diagram 9 shares losses with the holders of profit-sharing investment accounts. As the equity of the banking system does not bear all of the losses, its ability to continue to lend is less impaired than in the conventional finance scenario.

Similarly, the issuer of a sukuk based on a mudharaba contract, as in Diagram 7, is less exposed to corporate bankruptcy if the business faces a temporary decline than is the issuer of a conventional bond.

There are some prescribed situations such as UK financial services companies dealing with retail customers where the institution is required to "treat customers fairly." Absent such special cases, the underlying model of conventional finance is "caveat emptor" (let the buyer beware.) However Islam imposes on its adherents a requirement for ethical conduct at all times. Accordingly an Islamic bank should not "lend" money to customers if such "borrowing" is not in their best interests. This would for example apply to the provision of Shariah compliant housing finance to sub-prime borrowers who could not afford the cost once any low cost introductory period had elapsed.

This overarching requirement for ethical conduct may be the most powerful reason why an Islamic financial system is less likely to repeat the global financial crisis, as it protects against some of the behaviours that led to the crisis.

Follow @Mohammed_Amin