Serious writing for

serious readers

Summary

26 May 2011

This page comprises a chapter which I contributed to the book "Global Growth, Opportunities and Challenges in the Sukuk Market" edited by Sohail Jaffer and published by Euromoney Books. It is reproduced here by agreement with Euromoney.

It reviews how sukuk are accounted for under International Financial Reporting Standards (IFRS) and under the accounting standards promulgated by the Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI).

Both standards setting bodies have set out the purposes of financial accounting as they see them.

AAOIFI was established in 1991 and published "Statement of Financial Accounting No. 1: Objectives of Financial Accounting for Islamic Banks and Financial Institutions" in 1993. The introduction to that statement says:

"Financial accounting in Islam should be focused on the fair reporting of the entity's financial position and results of its operations, in a manner that would reveal what is halal (permissible) and haram (forbidden).

Section 6/2 of the standard sets out the objectives of financial reports in six paragraphs which the first is:

"Information about the Islamic bank’s compliance with the Islamic Shari’a and its objectives and to establish such compliance; and information establishing the separation of prohibited earnings and expenditures, if any, which occurred, and of the manner in which these were disposed of."

IFRS are published by the International Accounting Standards Board (IASB). In 2001 the IASB adopted its "Framework for the Preparation and Presentation of Financial Statements." Paragraph 12 states:

"The objective of financial statements is to provide information about the financial position, performance and changes in financial position of an entity that is useful to a wide range of users in making economic decisions.”

In paragraph 33 and 34 the framework emphasises the need to faithfully represent the transactions that have taken place:

To be reliable, information must represent faithfully the transactions and other events it either purports to represent or could reasonably be expected to represent. Thus, for example, a balance sheet should represent faithfully the transactions and other events that result in assets, liabilities and equity of the entity at the reporting date which meet the recognition criteria.

Most financial information is subject to some risk of being less than a faithful representation of that which it purports to portray. This is not due to bias, but rather to inherent difficulties either in identifying the transactions and other events to be measured or in devising and applying measurement and presentation techniques that can convey messages that correspond with those transactions and events. In certain cases, the measurement of the financial effects of items could be so uncertain that entities generally would not recognise them in the financial statements; for example, although most entities generate goodwill internally over time, it is usually difficult to identify or measure that goodwill reliably. In other cases, however, it may be relevant to recognise items and to disclose the risk of error surrounding their recognition and measurement.

Paragraph 35 emphasises the importance of substance over form:

If information is to represent faithfully the transactions and other events that it purports to represent, it is necessary that they are accounted for and presented in accordance with their substance and economic reality and not merely their legal form. The substance of transactions or other events is not always consistent with that which is apparent from their legal or contrived form. For example, an entity may dispose of an asset to another party in such a way that the documentation purports to pass legal ownership to that party; nevertheless, agreements may exist that ensure that the entity continues to enjoy the future economic benefits embodied in the asset. In such circumstances, the reporting of a sale would not represent faithfully the transaction entered into (if indeed there was a transaction).

The above quotations illustrate that the two standard-setting organisations have different priorities. The implications will be seen when the accounting for sukuk transactions is considered in detail. As accounting issues are much easier to understand when illustrative numbers are available, this chapter considers two transaction scenarios.

Before considering an illustrative sukuk transaction, it is helpful to consider the case of a hypothetical company, Trader plc which makes a conventional public bond issue with the following terms and consequential cash flows:

| Illustrative public bond issue transaction summary | ||

| Date | Transactions | Cash paid |

| 1 January 2011 | Trader plc issues corporate bonds to investors | 100.00 |

| Annual interest 5% | ||

| Bonds repayable in five years time for £110 | ||

| Bonds secured on Trader plc's office building | ||

| The internal rate of return on the loan is approximately 6.477% | ||

| 31 December 2011 | Trader plc pays interest to bond investors | 5.00 |

| 31 December 2012 | Trader plc pays interest to bond investors | 5.00 |

| 31 December 2013 | Trader plc pays interest to bond investors | 5.00 |

| 31 December 2014 | Trader plc pays interest to bond investors | 5.00 |

| 31 December 2015 | Trader plc pays interest to bond investors | 5.00 |

| Trader plc pays investors to repay the bond | 110.00 | |

Note that Trader plc is due to repay £110 when the bond matures even though only £100 was borrowed. Accordingly over the five years Trader plc incurs a total cost of £35 (five annual payments of £5 plus the premium on redemption of £10) as the cost of borrowing the £100. This aggregate cost needs to be spread over the five years in the most appropriate manner. IFRS requires one to compute an annual cost of funds to apply to the amount owed. An internal rate of return calculation will show this to be approximately 6.477%. Under accruals accounting, Trader plc is required to recognise an initial bond liability of £100 which is then amortised upward toward the redemption amount as illustrated in the bond liability table below.

| Bond liability table | ||||

| Year | Bond liability b/f |

Interest on opening balance at approximately 6.477% | Cash paid | Bond liability c/f |

| 2011 | 100.00 | 6.75 | 5.00 | 101.75 |

| 2012 | 101.75 | 6.87 | 5.00 | 103.62 |

| 2013 | 103.62 | 6.99 | 5.00 | 105.61 |

| 2014 | 105.61 | 7.13 | 5.00 | 107.74 |

| 2015 | 107.74 | 7.26 | 5.00 | 110.00 |

In order to present a complete set of accounts for Trader plc, some assumptions are required regarding its other financial numbers. The following have been assumed:

These assumptions give rise to the following income statement, cash flow statement and balance sheet for Trader plc over the five year life of the bond.

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Income statement |

|

|

|

|

|

Operating income |

250.00 |

250.00 |

250.00 |

250.00 |

250.00 |

Interest expense |

-6.75 |

-6.87 |

-6.99 |

-7.13 |

-7.26 |

Net profit |

243.25 |

243.13 |

243.01 |

242.87 |

242.74 |

Distribution to shareholders |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

Retained profit |

- |

- |

- |

- |

- |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Cash flow statement |

|

|

|

|

|

Operating income |

250.00 |

250.00 |

250.00 |

250.00 |

250.00 |

Interest expense |

-6.75 |

-6.87 |

-6.99 |

-7.13 |

-7.26 |

Add back non-cash interest expense |

1.75 |

1.87 |

1.99 |

2.13 |

2.26 |

Net cash generated by operating activities |

245.00 |

245.00 |

245.00 |

245.00 |

245.00 |

|

|

|

|

|

|

Financing transactions |

|

|

|

|

|

Proceeds from issue of bonds |

100.00 |

|

|

|

|

Dividends paid to owners of the company |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

Cash used to redeem bonds |

|

|

|

|

-110.00 |

Net cash from financing activities |

-143.25 |

-243.13 |

-243.01 |

-242.87 |

-352.74 |

|

|

|

|

|

|

Net increase in cash |

101.75 |

1.87 |

1.99 |

2.13 |

-107.74 |

Cash at the beginning of the year |

25.00 |

126.75 |

128.62 |

130.61 |

132.74 |

Cash at the end of the year |

126.75 |

128.62 |

130.61 |

132.74 |

25.00 |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Balance sheet |

|

|

|

|

|

Building |

100.00 |

100.00 |

100.00 |

100.00 |

100.00 |

Other operating assets |

350.00 |

350.00 |

350.00 |

350.00 |

350.00 |

Cash |

126.75 |

128.62 |

130.61 |

132.74 |

25.00 |

Total assets |

576.75 |

578.62 |

580.61 |

582.74 |

475.00 |

|

|

|

|

|

|

Financed by: |

|

|

|

|

|

Shareholders equity |

475.00 |

475.00 |

475.00 |

475.00 |

475.00 |

Bond liability |

101.75 |

103.62 |

105.61 |

107.74 |

- |

|

576.75 |

578.62 |

580.61 |

582.74 |

475.00 |

There is no purpose in preparing any accounts under AAOIFI accounting standards for this bond issue scenario. AAOIFI is not concerned with companies that engage in conventional financial transactions.

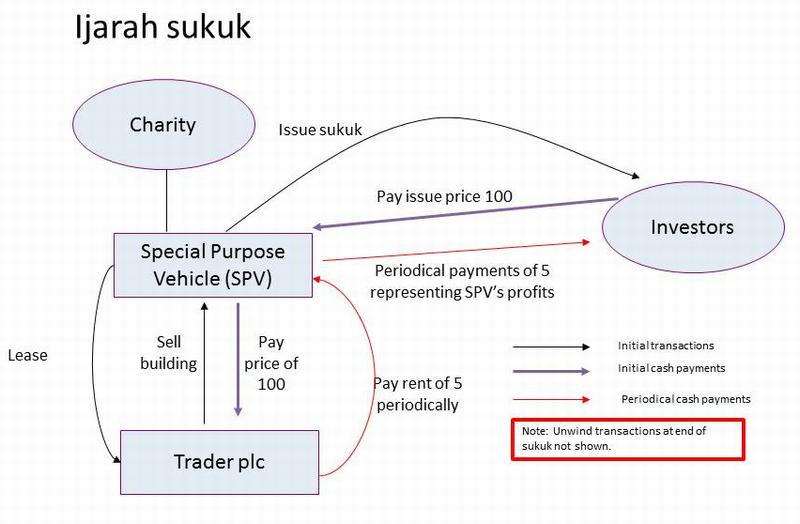

Instead of the bond issue above, assume now that Trader plc obtains £100 of finance by issuing sukuk. The sukuk transaction is designed to replicate the economics of the conventional bond transaction from the perspective of Trader plc. Its details and the associated cash flows are set out below. (SPV is a Special Purpose Vehicle, a company set up specifically for this sukuk transaction, which is normally owned by a charity.)

| Date | Transactions | Cash paid |

| 1 January 2011 | Trader plc sells office building to SPV | 100.00 |

| Trader plc agrees to repurchase building in five years time for £110 | ||

| SPV leases office building to Trader plc for £5 pa | ||

| Sukuk investors subscribe for sukuk issued by SPV | 100.00 | |

| SPV holds building on trust for sukuk investors | ||

| Trusteeship fee set at £0.02 pa | ||

| SPV has £0.01 of paid in capital prior to sukuk transaction | ||

| 31 December 2011 | Trader plc pays rent to SPV | 5.00 |

| SPV charge made to trust | 0.02 | |

| SPV pays operating costs | 0.01 | |

| SPV dividend distribution to charity | 0.01 | |

| SPV cash distribution to investors | 4.98 | |

| 31 December 2012 | Trader plc pays rent to SPV | 5.00 |

| SPV charge made to trust | 0.02 | |

| SPV pays operating costs | 0.01 | |

| SPV dividend distribution to charity | 0.01 | |

| SPV cash distribution to investors | 4.98 | |

| 31 December 2013 | Trader plc pays rent to SPV | 5.00 |

| SPV charge made to trust | 0.02 | |

| SPV pays operating costs | 0.01 | |

| SPV dividend distribution to charity | 0.01 | |

| SPV cash distribution to investors | 4.98 | |

| 31 December 2014 | Trader plc pays rent to SPV | 5.00 |

| SPV charge made to trust | 0.02 | |

| SPV pays operating costs | 0.01 | |

| SPV dividend distribution to charity | 0.01 | |

| SPV cash distribution to investors | 4.98 | |

| 31 December 2015 | Trader plc pays rent to SPV | 5.00 |

| SPV charge made to trust | 0.02 | |

| SPV pays operating costs | 0.01 | |

| Trader plc pays SPV cost of repurchasing office building | 110.00 | |

| SPV dividend distribution to charity | 0.01 | |

| SPV cash distribution to investors | 114.98 |

From Trader plc's perspective the cash flows under the sukuk transaction are identical to the cash flows under the bond. To ensure this, the minor costs of selling the building to the SPV have been ignored.

SPV has some real costs of its own, even though they are small, and here they have been assumed to be equivalent to one basis point. The transaction also assumes that SPV is to make a profit of one basis point which it will distribute to the charity which is its shareholder so the total cost to the investors from the use of a sukuk structure is two basis points as compared with the bond issue scenario.

While this article is about accounting rather than Shariah, the statement of the AAOIFI Shariah board in February 2008 addresses in section five the buyback of the building:

Fifth: It is permissible for a lessee in a Sukuk al-Ijarah to undertake to purchase the leased assets when the Sukuk are extinguished for its nominal value, provided he {lessee} is not also a partner, Mudarib, or investment agent.

This permission of a fixed price buyback of the building where the sukuk structure involves an ijarah contract is the reason that most sukuk now use ijarah; it enables the guarantee of a fixed predetermined return to the sukuk investors provided that Trader plc remained solvent so that it can honour its obligations to pay rent and to repurchase the building.

The above diagram shows the sukuk structure with the initial and periodical cash flows. The unwind transactions are not shown. This diagram was created specifically for this website article, and was not present in the published book chapter for space reasons.

Under IFRS, one is required to consider the economic substance of the transactions.

From the perspective of Trader plc, under the sukuk transaction it receives £100, is required to pay five annual rental payments of £5 and to pay £110 at the end of the transaction when legal title to the building will be returned to Trader plc. The repurchase price of £110 is fixed regardless of whether the building soars in value or whether its value reduces. Accordingly, Trader plc is fully exposed to all changes in the economic value of the building. This means that under IFRS the sukuk transaction is regarded purely as a financing transaction; Trader plc recognises a financial liability in respect of the sukuk while retaining the building on its balance sheet even though Trader plc does not own it during the life of the sukuk transaction. The precise accounting terminology is that Trader plc does not "de-recognise" the building.

Trader plc will therefore prepare the following accounts under IFRS:

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

Income statement |

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

|

|

|

|

|

|

Operating income |

250.00 |

250.00 |

250.00 |

250.00 |

250.00 |

Financing expense under sukuk transaction |

-6.75 |

-6.87 |

-6.99 |

-7.13 |

-7.26 |

Net profit |

243.25 |

243.13 |

243.01 |

242.87 |

242.74 |

Distribution to shareholders |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

Retained profit |

- |

- |

- |

- |

- |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Cash flow statement |

|

|

|

|

|

Operating income |

250.00 |

250.00 |

250.00 |

250.00 |

250.00 |

Financing expense under sukuk transaction |

-6.75 |

-6.87 |

-6.99 |

-7.13 |

-7.26 |

Add back non-cash financing expense |

1.75 |

1.87 |

1.99 |

2.13 |

2.26 |

Net cash generated by operating activities |

245.00 |

245.00 |

245.00 |

245.00 |

245.00 |

|

|

|

|

|

|

Financing transactions |

|

|

|

|

|

Proceeds from sukuk financing transaction |

100.00 |

|

|

|

|

Dividends paid to owners of the company |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

Payment of sukuk financing obligation |

|

|

-110.00 |

||

Net cash from financing activities |

-143.25 |

-243.13 |

-243.01 |

-242.87 |

-352.74 |

|

|

|

|

|

|

Net increase in cash |

101.75 |

1.87 |

1.99 |

2.13 |

-107.74 |

Cash at the beginning of the year |

25.00 |

126.75 |

128.62 |

130.61 |

132.74 |

Cash at the end of the year |

126.75 |

128.62 |

130.61 |

132.74 |

25.00 |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Balance sheet |

|

|

|

|

|

Building |

100.00 |

100.00 |

100.00 |

100.00 |

100.00 |

Other operating assets |

350.00 |

350.00 |

350.00 |

350.00 |

350.00 |

Cash |

126.75 |

128.62 |

130.61 |

132.74 |

25.00 |

Total assets |

576.75 |

578.62 |

580.61 |

582.74 |

475.00 |

|

|

|

|

|

|

Financed by: |

|

|

|

|

|

Shareholders equity |

475.00 |

475.00 |

475.00 |

475.00 |

475.00 |

Liability under sukuk financing transaction |

101.75 |

103.62 |

105.61 |

107.74 |

- |

|

576.75 |

578.62 |

580.61 |

582.74 |

475.00 |

Footnote disclosure for Trader plc balance sheet

On 1 January 2011 Trader plc entered into a sukuk financing transaction by selling the building to an SPV for £100 and leasing it back for five years at an annual rent of £5 pa. Trader plc is obligated to repurchase the building for £110 on 31 December 2015. As Trader plc retains all of the risks and rewards in relation to the building, the transaction has been accounted for as a financing transaction and the building has not been derecognised from Trader plc's balance sheet. The effective cost of finance under the sukuk transaction is approximately 6.477%.

SPV is a company and is itself also obliged to prepare accounts. These will be as follows:

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

Income statement |

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Operating income (trusteeship charge) |

0.02 |

0.02 |

0.02 |

0.02 |

0.02 |

Operating expenses |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

Net profit |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

Distribution to shareholders |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

Retained profit |

- |

- |

- |

- |

- |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Cash flow statement |

|

|

|

|

|

Net cash generated by operating activities |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

|

|

|

|

|

|

Financing transactions |

|

|

|

|

|

Dividends paid to owners of the company |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

Net cash from financing activities |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

|

|

|

|

|

|

Net increase in cash |

- |

- |

- |

- |

- |

Cash at the beginning of the year |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

Cash at the end of the year |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Balance sheet |

|

|

|

|

|

Cash |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

|

|

|

|

|

|

Shareholders funds |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

Footnote disclosure for SPV balance sheet

SPV acts a trustee in respect of sukuk financing transaction initiated by Trader plc. Under this transaction, SPV holds the legal title to a building on trust, with the beneficial interest being held by the owners of the sukuk instruments. As SPV is acting only as a trustee, the building and the cash flows arising from it are not shown on SPV's balance sheet. Accordingly, SPV accounts only for its trusteeship fee and its own operating expenses and dividends paid to the charity which is SPV's sole shareholder.

It will be seen that Trader plc’s financial statements have identical numbers to the bond issue scenario. That is to be expected as Trader plc’s cash flows under the sukuk transaction are identical to its cash flows under the conventional bond transaction. As both transactions have the same economic consequences for Trader plc, under IFRS they receive almost identical accounting treatment, since the goal of IFRS is to reflect the substance of the transactions undertaken.

The text descriptions are slightly different to recognise the fact that although Trader plc's payments to sukuk holders in excess of the amount they subscribed for the sukuk are regarded as a financial expense, they are not interest. Furthermore, Trader plc gives details of the sukuk financing transaction in the notes to the financial statements so that investors are not misled by the fact that the building is included on Trader plc's balance sheet even though it is not owned.

Although SPV owns the building, it is held in trust for the sukuk investors and is not beneficially owned by SPV. Accordingly SPV does not include the building as an asset on its balance sheet. Similarly the sukuk are not a liability of SPV; they represent the investors’ beneficial interest in the building which is held on trust for them by SPV.

AAOIFI does not have a specific accounting standard for sukuk.

Unlike IFRS, "Statement of Financial Accounting No. 1: Objectives of Financial Accounting for Islamic Banks and Financial Institutions" mentioned above does not have any overriding concept of substance. Nor does "Statement of Financial Accounting No. 2 (Amended): Concepts of Financial Accounting for Islamic Banks and Financial Institutions" also adopted in 1993.

However AAOIFI has recently redrafted these statements in July 2010 to take account of substance, to give it recognition in addition to recognising the importance of the legal form of the contract. However, there is an overriding requirement to make sure that if substance and form are in conflict Shariah shall prevail.

Given the importance of demonstrating to the users of the accounts that the transactions comply with Shariah, in the writer’s opinion under AAOIFI the financial statements would be prepared as below. The key differences between the following AAOIFI accounts and the IFRS accounts are as follows:

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

Income statement |

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

|

|

|

|

|

|

Operating income |

250.00 |

250.00 |

250.00 |

250.00 |

250.00 |

Rent |

-5.00 |

-5.00 |

-5.00 |

-5.00 |

-5.00 |

Net profit |

245.00 |

245.00 |

245.00 |

245.00 |

245.00 |

Distribution to shareholders |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

Retained profit |

1.75 |

1.87 |

1.99 |

2.13 |

2.26 |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Cash flow statement |

|

|

|

|

|

Operating income |

245.00 |

245.00 |

245.00 |

245.00 |

245.00 |

Net cash generated by operating activities |

245.00 |

245.00 |

245.00 |

245.00 |

245.00 |

|

|

|

|

|

|

Investing activities |

|

|

|

|

|

Proceeds from sale of building |

100.00 |

|

|

|

|

Purchase of building |

|

|

|

|

-110.00 |

Net cash from (used in) investing activities |

100.00 |

- |

- |

- |

-110.00 |

|

|

|

|

|

|

Financing transactions |

|

|

|

|

|

Dividends paid to owners of the company |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

Net cash from financing activities |

-243.25 |

-243.13 |

-243.01 |

-242.87 |

-242.74 |

|

|

|

|

|

|

Net increase in cash |

101.75 |

1.87 |

1.99 |

2.13 |

-107.74 |

Cash at the beginning of the year |

25.00 |

126.75 |

128.62 |

130.61 |

132.74 |

Cash at the end of the year |

126.75 |

128.62 |

130.61 |

132.74 |

25.00 |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Balance sheet |

|

|

|

|

|

Building |

- |

- |

- |

- |

110.00 |

Other operating assets |

350.00 |

350.00 |

350.00 |

350.00 |

350.00 |

Cash |

126.75 |

128.62 |

130.61 |

132.74 |

25.00 |

Total assets |

476.75 |

478.62 |

480.61 |

482.74 |

485.00 |

|

|

|

|

|

|

Financed by: |

|

|

|

|

|

Shareholders equity b/f |

475.00 |

476.75 |

478.62 |

480.61 |

482.74 |

Retained profit of current year |

1.75 |

1.87 |

1.99 |

2.13 |

2.26 |

|

476.75 |

478.62 |

480.61 |

482.74 |

485.00 |

SPV's will also prepare its own accounts under AAOIFI

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

Income statement |

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Operating income (trusteeship charge) |

0.02 |

0.02 |

0.02 |

0.02 |

0.02 |

Operating expenses |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

Net profit |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

Distribution to shareholders |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

Retained profit |

- |

- |

- |

- |

- |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Cash flow statement |

|

|

|

|

|

Net cash generated by operating activities |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

|

|

|

|

|

|

Financing transactions |

|

|

|

|

|

Dividends paid to owners of the company |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

Net cash from financing activities |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

-0.01 |

|

|

|

|

|

|

Net increase in cash |

- |

- |

- |

- |

- |

Cash at the beginning of the year |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

Cash at the end of the year |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Balance sheet |

|

|

|

|

|

Cash |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

|

|

|

|

|

|

Shareholders funds |

0.01 |

0.01 |

0.01 |

0.01 |

0.01 |

Accounts should also be prepared for the sukuk investment fund for which the SPV is a trustee

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Statement of operations |

|

|

|

|

|

Rental income |

5.00 |

5.00 |

5.00 |

5.00 |

5.00 |

Gain from sale of building |

|

|

|

10.00 |

|

Net income before the mudarib's share |

5.00 |

5.00 |

5.00 |

5.00 |

15.00 |

Mudarib's share |

-0.02 |

-0.02 |

-0.02 |

-0.02 |

-0.02 |

Net income after the mudarib's share |

4.98 |

4.98 |

4.98 |

4.98 |

14.98 |

Distribution to sukuk holders |

-4.98 |

-4.98 |

-4.98 |

-4.98 |

-14.98 |

Net income retained |

- |

- |

- |

- |

- |

|

Year ended |

Year ended |

Year ended |

Year ended |

Year ended |

|

31/12/2011 |

31/12/2012 |

31/12/2013 |

31/12/2014 |

31/12/2015 |

Balance sheet |

|

|

|

|

|

Building |

100.00 |

100.00 |

100.00 |

100.00 |

- |

|

|

|

|

|

|

Sukuk investors stake in investment fund |

100.00 |

100.00 |

100.00 |

100.00 |

|

Footnote

When the building was sold on 31/12/2015, the entire sale proceeds of £110 were distributed to the sukuk holders as the investment fund was dissolved at that time.

In the writer’s view, as well as preparing its own accounts as SPV, accounts should be prepared for the investment fund represented by the sukuk in accordance with Financial Accounting Standard 14 "Investment Funds" and that these are also shown above.

For comparability, Trader plc is shown as distributing only the same amount of profit each year as a dividend to its shareholders as it distributes under IFRS accounting. (The amount to distribute is a management decision and Trader plc is not required to distribute all of its post tax profit.) Accordingly, Trader plc's cash balances are the same as under the IFRS scenario. The key difference is that over the five-year period Trader plc records £10 less in total expenses and at the end of the period it reports the purchase of the building for £110 whereas under IFRS the building remains on Trader plc's balance sheet throughout at £100.

This is not a meaningful question. IFRS and AAOIFI accounting have different objectives and perspectives.

IFRS analyses the sukuk transaction entirely on the basis of its economic substance and sees it as a financing transaction. Fundamentally, this derives from the requirement to repurchase the building at a fixed price irrespective of the market value.

As an alternative, if the sukuk transaction required Trader plc to repurchase the building at the open market value on the date of repurchase (which totally changes the economics of the transaction) then Trader plc would record only £5 of rental expense each year, and it would de-recognise the building when sold to the SPV since from that point Trader plc would have no economic exposure to value changes in the building.

The main purpose of AAOIFI accounting is to satisfy the religious needs of the users of the accounts. Accordingly AAOIFI does not allow substance to determine the presentation of the accounts but instead gives significant weight to the legal form of contracts and Shariah requirements are overriding.

When AAOIFI was established, global accounting was very fragmented. Although international accounting standards existed, most countries required the use of local accounting standards and in the countries of the Gulf accounting standards were nascent or non-existent. Accordingly AAOIFI played an important standard setting role in the Islamic finance industry at that time.

In 2010 the picture is very different. Outside a few countries in the Gulf and the USA, virtually the entire world accounts under IFRS. The last significant holdout is USA but there is a convergence project between the US Financial Accounting Standards Board and the IASB to converge IFRS and US GAAP (Generally Accepted Accounting Principles). Accordingly, Islamic financial institutions in all parts of the world apart from some Gulf countries will be accounting under IFRS very shortly if they do not already do so.

In these circumstances, there is little point in AAOIFI continuing to promulgate accounting standards. Instead, it should focus on Shariah standards where AAOIFI's role is critical. As far as accounting is concerned, AAOIFI should encourage the IASB to ensure that the needs of Islamic users of financial statements are met by IFRS. This would include such matters as additional footnote disclosures so that investors knew what proportion of a company's dividend payments represented impure income, what part of its retained earnings were impure and which of the company's assets were liable to Zakah. Islamic investors would like to have such information in respect of the financial statements of all publicly traded companies, with the exception of those companies carrying on wholly prohibited activities such as alcohol distribution.

Follow @Mohammed_Amin