Serious writing for

serious readers

Summary

25 March 2011

Most non-Muslims know very little about Islamic finance. There have been several press stories recently implying that the UK Government is giving some kind of unfair benefit to Muslims by changing UK tax law to facilitate Islamic finance. At the same time, many Muslims also have difficulty understanding Islamic finance and are surprised when they learn that it is usually more expensive than conventional finance.

This page covers one form of financial product, the provision of finance to an individual to purchase a property. This could be their private residence, or it could be property that is rented on to tenants, whether commercial or residential.

Everything is considered from the customer’s perspective. The issues are often much more complex when considered from the perspective of the institution providing the finance.

There is a downloadable PDF version.

Before looking at Islamic finance, it is important to be clear how conventional mortgages work. They fall into two main types.

In this case, the price of the money being lent is fixed for the entire duration of the mortgage. For example a property costing £500,000 may be financed under the following terms.

Cost of property from third party |

£500,000 |

Term of finance |

25 years |

Customer deposit required |

25% which is £125,000 |

Amount of loan |

£375,000 |

Interest rate |

5% pa fixed |

Frequency of customer payments |

Once a year on the anniversary of the making of the loan. |

Customer to make equal annual payments |

|

Note: The payment frequency would normally be monthly. Annual payments are used purely for illustration to reduce the number of rows on the table of figures.

The customer needs to make 25 annual payments of £26,607. Table A below shows the complete calculations.

| Table A - Conventional fixed rate mortgage | ||||

| Year | Amount owed at start of year | Interest charge | Repayment | Amount owed at end of year |

| 1 | 375,000 | 18,750 | 26,607 | 367,143 |

| 2 | 367,143 | 18,357 | 26,607 | 358,892 |

| 3 | 358,892 | 17,945 | 26,607 | 350,230 |

| 4 | 350,230 | 17,512 | 26,607 | 341,135 |

| 5 | 341,135 | 17,057 | 26,607 | 331,585 |

| 6 | 331,585 | 16,579 | 26,607 | 321,556 |

| 7 | 321,556 | 16,078 | 26,607 | 311,027 |

| 8 | 311,027 | 15,551 | 26,607 | 299,971 |

| 9 | 299,971 | 14,999 | 26,607 | 288,363 |

| 10 | 288,363 | 14,418 | 26,607 | 276,173 |

| 11 | 276,173 | 13,809 | 26,607 | 263,375 |

| 12 | 263,375 | 13,169 | 26,607 | 249,937 |

| 13 | 249,937 | 12,497 | 26,607 | 235,827 |

| 14 | 235,827 | 11,791 | 26,607 | 221,010 |

| 15 | 221,010 | 11,051 | 26,607 | 205,454 |

| 16 | 205,454 | 10,273 | 26,607 | 189,120 |

| 17 | 189,120 | 9,456 | 26,607 | 171,969 |

| 18 | 171,969 | 8,598 | 26,607 | 153,959 |

| 19 | 153,959 | 7,698 | 26,607 | 135,050 |

| 20 | 135,050 | 6,753 | 26,607 | 115,196 |

| 21 | 115,196 | 5,760 | 26,607 | 94,348 |

| 22 | 94,348 | 4,717 | 26,607 | 72,458 |

| 23 | 72,458 | 3,623 | 26,607 | 49,474 |

| 24 | 49,474 | 2,474 | 26,607 | 25,341 |

| 25 | 25,341 | 1,267 | 26,607 | 0 |

| 290,182 | 665,182 | |||

The customer borrows £375,000 and over the 25 years pays back a total of £665,182 being the principal borrowed of £375,000 and total interest of £290,182.

Such long term fixed rate mortgages are relatively uncommon in the UK. However in the USA a 30 year fixed rate mortgage is very common.

UK lenders typically prefer to make variable rate loans, as this allows an easier match between the lender’s own funding and the mortgage loan advanced. The variable rate can either be linked to an external rate, e.g. Bank of England rate + 0.5%, or it can be an administered rate which is set by the lender, e.g. the XYZ Building Society’s standard variable interest rate.

Variable rate mortgages fall into two main types.

The customer makes level regular repayments which are calculated to pay off the loan by the maturity date, based upon the current level of the variable interest rate. If the interest rate changes, the customer’s repayments are recomputed.

For example consider a variable rate repayment mortgage with the following terms:

Cost of property from third party |

£500,000 |

Term of finance |

25 years |

Customer deposit required |

25% which is £125,000 |

Amount of loan |

£375,000 |

Interest rate |

XYZ Building Society’s standard variable rate, currently 5% |

Interest adjustment dates |

The interest rate can only be adjusted at the end of each year. |

Frequency of customer payments |

Once a year on the anniversary of the making of the loan. |

Customer to make equal annual payments |

|

Note: The payment frequency would normally be monthly. Annual payments are used purely for illustration to reduce the number of rows on the table of figures. Similarly the interest would be adjustable more frequently than annually, typically monthly or even daily.

To illustrate the numbers, assume that the XYZ Building Society’s standard variable rate remains 5% for the first 3 years, then becomes 4% until the end of year 7, than rises to 6% until the end of year 15, then falls to 5% until the end of year 22, and then becomes 4% until the redemption date at year 25.

Table B below shows the numbers; the customer’s annual repayments go up and down as the interest rate changes, but in every case are calculated to repay the loan by the end of year 25 on the assumption that there are no further changes in interest rate.

| Table B - floating rate repayment mortgage | ||||||

| Year | Amount owed at start of year | Interest charge | Repayment | Amount owed at end of year | Interest rate for year | |

| 1 | 375,000 | 18,750 | 26,607 | 367,143 | 5% | |

| 2 | 367,143 | 18,357 | 26,607 | 358,892 | 5% | |

| 3 | 358,892 | 17,945 | 26,607 | 350,230 | 5% | |

| 4 | 350,230 | 14,009 | 24,236 | 340,004 | 4% | |

| 5 | 340,004 | 13,600 | 24,236 | 329,368 | 4% | |

| 6 | 329,368 | 13,175 | 24,236 | 318,308 | 4% | |

| 7 | 318,308 | 12,732 | 24,236 | 306,804 | 4% | |

| 8 | 306,804 | 18,408 | 28,335 | 296,877 | 6% | |

| 9 | 296,877 | 17,813 | 28,335 | 286,354 | 6% | |

| 10 | 286,354 | 17,181 | 28,335 | 275,200 | 6% | |

| 11 | 275,200 | 16,512 | 28,335 | 263,376 | 6% | |

| 12 | 263,376 | 15,803 | 28,335 | 250,844 | 6% | |

| 13 | 250,844 | 15,051 | 28,335 | 237,559 | 6% | |

| 14 | 237,559 | 14,254 | 28,335 | 223,478 | 6% | |

| 15 | 223,478 | 13,409 | 28,335 | 208,552 | 6% | |

| 16 | 208,552 | 10,428 | 27,009 | 191,971 | 5% | |

| 17 | 191,971 | 9,599 | 27,009 | 174,561 | 5% | |

| 18 | 174,561 | 8,728 | 27,009 | 156,281 | 5% | |

| 19 | 156,281 | 7,814 | 27,009 | 137,086 | 5% | |

| 20 | 137,086 | 6,854 | 27,009 | 116,932 | 5% | |

| 21 | 116,932 | 5,847 | 27,009 | 95,770 | 5% | |

| 22 | 95,770 | 4,789 | 27,009 | 73,551 | 5% | |

| 23 | 73,551 | 2,942 | 26,504 | 49,989 | 4% | |

| 24 | 49,989 | 2,000 | 26,504 | 25,485 | 4% | |

| 25 | 25,485 | 1,019 | 26,504 | - | 4% | |

| 297,019 | 672,019 | |||||

The aggregate interest paid in Table B exceeds that in Table A because of the different assumptions made regarding the level of the interest rate at different points in time.

In this case, the customer is only required to make payments of interest. The customer has flexibility to make capital repayments when he wishes, and in any event must repay the full loan on the repayment date if it has not been repaid beforehand. For example:

Cost of property from third party |

£500,000 |

Term of finance |

25 years |

Customer deposit required |

25% which is £125,000 |

Amount of loan |

£375,000 |

Interest rate |

XYZ Building Society’s standard variable rate, currently 5% |

Interest adjustment dates |

The interest rate can only be adjusted at the end of each year. |

Frequency of customer interest payments |

Once a year on the anniversary of the making of the loan. |

Customer has discretion when to make capital repayments |

|

As the lender is taking the risk that the customer will pay off no capital until year 25, it has a greater risk exposure than with a repayment mortgage where the amount of debt outstanding reduces over the life of the loan. Accordingly lenders typically only offer interest only mortgages to their more creditworthy customers.

There is no point producing a table of figures for an interest only loan, as the pattern depends critically on how much the customer chooses to repay before maturity and when he chooses to make those pre-maturity payments. If the customer pays off no capital until year 25, on the repayment date he must find £375,000 to repay the loan in full.

The purpose of Islamic finance, as found in practice, is to replicate the economics of the above conventional mortgages while remaining compliant with Shariah.

It would also be possible to devise Shariah compliant property finance contracts that had different economics, for example by having the Islamic bank share in any increase in value of the property, but such contracts are uncommon for reasons connected with the bank’s risk management and also due to customer demands. Such alternative contracts are beyond the scope of this simple introduction.

There are two main contracts used.

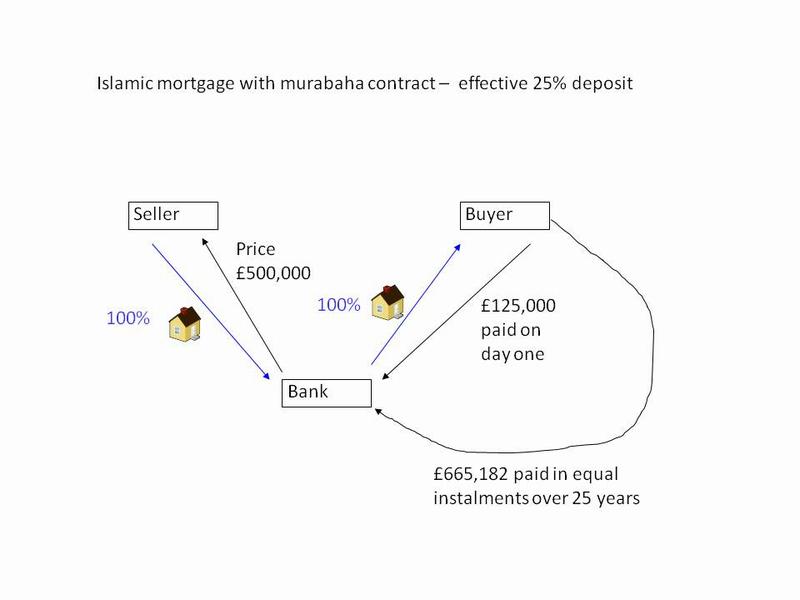

Assume that a property whose price from the third party is £500,000 is to be purchased on with Shariah compliant finance. The Islamic bank will buy the property for £500,000 having pre-agreed with the customer that the customer will then buy the property from the Islamic bank at a pre-agreed price, on pre-agreed payment terms.

The Islamic bank may offer finance to the customer on the following terms:

Cost of property from third party |

£500,000 |

Term of finance |

25 years |

Islamic bank will purchase the property and immediately resell it to the customer for a fixed price: |

£790,182 |

Part of price payable by customer on day one |

£125,000 |

Balance of price to be paid in 25 equal installments |

£665,182 |

Frequency of customer installments |

Once a year on the anniversary of the initial purchase |

Note: The payment frequency would normally be monthly. Annual payments are used purely for illustration to reduce the number of rows on the table of figures.

The contract is illustrated in the following diagram.

Table C below shows the customer’s payments to the Islamic bank and the amount of purchase price outstanding at any time. The total cost of the finance is £290,182 since the customer ends up paying a total price of £790,182 for a house that he could have bought for £500,000 if he had that amount of money available on day one.

| Table C - Murabaha property finance | ||||

| Year | Amount owed to Islamic bank for the purchase of the property | Customer part payment on day one | Customer's annual part payment | Amount owed to Islamic bank at end of year |

| 1 | 790,182 | 125,000 | 26,607 | 638,575 |

| 2 | 638,575 | 26,607 | 611,967 | |

| 3 | 611,967 | 26,607 | 585,360 | |

| 4 | 585,360 | 26,607 | 558,753 | |

| 5 | 558,753 | 26,607 | 532,146 | |

| 6 | 532,146 | 26,607 | 505,538 | |

| 7 | 505,538 | 26,607 | 478,931 | |

| 8 | 478,931 | 26,607 | 452,324 | |

| 9 | 452,324 | 26,607 | 425,717 | |

| 10 | 425,717 | 26,607 | 399,109 | |

| 11 | 399,109 | 26,607 | 372,502 | |

| 12 | 372,502 | 26,607 | 345,895 | |

| 13 | 345,895 | 26,607 | 319,288 | |

| 14 | 319,288 | 26,607 | 292,680 | |

| 15 | 292,680 | 26,607 | 266,073 | |

| 16 | 266,073 | 26,607 | 239,466 | |

| 17 | 239,466 | 26,607 | 212,859 | |

| 18 | 212,859 | 26,607 | 186,251 | |

| 19 | 186,251 | 26,607 | 159,644 | |

| 20 | 159,644 | 26,607 | 133,037 | |

| 21 | 133,037 | 26,607 | 106,429 | |

| 22 | 106,429 | 26,607 | 79,822 | |

| 23 | 79,822 | 26,607 | 53,215 | |

| 24 | 53,215 | 26,607 | 26,608 | |

| 25 | 26,608 | 26,607 | 0 | |

| 665,182 | ||||

From the perspective of each of the customer and the financial institution, the cash flows are identical to the cash flows with the 25 year fixed rate mortgage discussed above. Accordingly the economics are the same, if the transaction proceeds for its full term. Hence the murabaha contract replicates a fixed rate mortgage.

However, there is a practical problem if the customer wants to sell the house to someone else and repay the Islamic bank, say at the end of three years. Under Table C, at the end of three years, the customer still owes £585,360 to the Islamic bank. (This compares with £350,230 owed on the same date with a conventional fixed rate mortgage.) It seems grossly unfair if the customer has to pay the bank £585,360 if he wishes to clear the debt at the end of year three. In economic terms, the Islamic bank will be making a windfall gain compared with the transaction running the full 25 years, since it is getting the money paid back early, with part of it being paid back 22 years early.

The logical thing would be for the bank to recompute the transaction to allow a discount for early payment. However I understand Shariah scholars do not allow the murabaha contract to contain early repayment provisions specifying how the bank will reduce the amount owed if the customer repays early. Instead the customer has to rely upon the Islamic bank reducing at its discretion the amount it demands for early repayment. Few customers regard that as satisfactory.

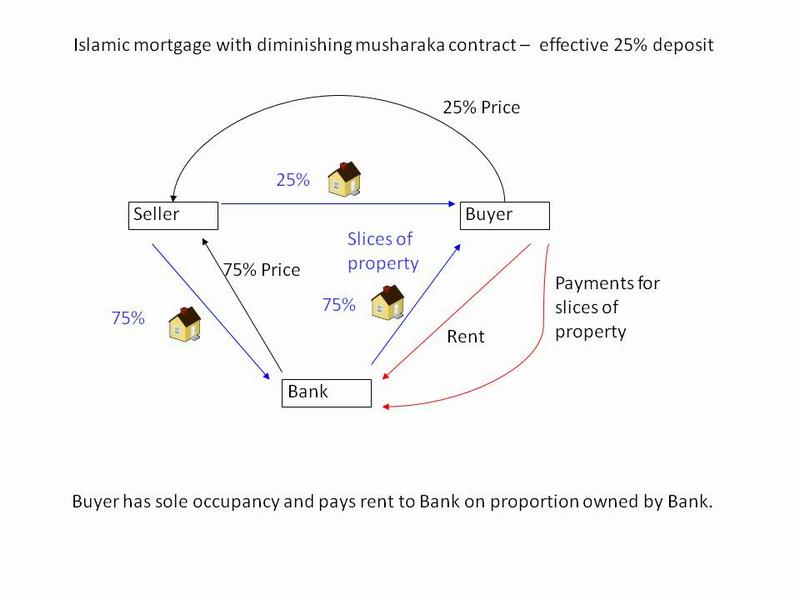

Under a diminishing musharaka contract, the customer and the Islamic bank purchase the property jointly under a musharaka contract, loosely a partnership contract as understood by Shariah law. The customer will have exclusive occupation, and will pay the Islamic bank rent on that part of the property which is owned by the Islamic bank. The transaction is called diminishing musharaka because the partnership shrinks as the customer buys out the bank and ends once the buyout process is completed.

The terms of the finance offer may be summarised as follows:

Cost of property from third party |

£500,000 |

Term of finance |

25 years |

Customer to initially purchase |

25%, costing £125,000 of the customer’s own money |

Bank to purchase |

75%, costing £375,000 of the bank’s money |

Rent calculation |

Rent to be calculated by multiplying the original cost of the part of the property owned by the bank by the XYZ Building Society’s standard variable interest rate, currently 5% |

Rental rate adjustment dates |

The rate can only be adjusted at the end of each year. |

Frequency of customer payments |

Once a year on the anniversary of the purchase from the third party. |

Price at which the customer will buy out the bank |

Price equal to the original cost to the bank |

Customer to make equal annual payments comprising both rent and part payments to acquire the bank’s share of the property. |

|

Note: The payment frequency would normally be monthly. Annual payments are used purely for illustration to reduce the number of rows on the table of figures.

The diagram below shows how the transaction operates.

To illustrate the numbers, assume that the XYZ Building Society’s standard variable rate remains 5% for the first 3 years, then becomes 4% until the end of year 7, than rises to 6% until the end of year 15, then falls to 5% until the end of year 22, and then becomes 4% until the redemption date at year 25.

Table D below shows the numbers; the customer’s annual repayments go up and down as the interest rate changes, but in every case are calculated to ensure that the customer has fully purchased the bank's share of the property by the end of year 25 on the assumption that there are no further changes in interest rate.

| Table D - diminishing musharaka contract | ||||||

| Year | Original cost of share of property owned by the bank at start of year | Rent charged | Cash from customer to pay rent and buy more of the property | Original cost of share of property owned by the bank at end of year | Interest rate used for rental calculation | |

| 1 | 375,000 | 18,750 | 26,607 | 367,143 | 5% | |

| 2 | 367,143 | 18,357 | 26,607 | 358,892 | 5% | |

| 3 | 358,892 | 17,945 | 26,607 | 350,230 | 5% | |

| 4 | 350,230 | 14,009 | 24,236 | 340,004 | 4% | |

| 5 | 340,004 | 13,600 | 24,236 | 329,368 | 4% | |

| 6 | 329,368 | 13,175 | 24,236 | 318,308 | 4% | |

| 7 | 318,308 | 12,732 | 24,236 | 306,804 | 4% | |

| 8 | 306,804 | 18,408 | 28,335 | 296,877 | 6% | |

| 9 | 296,877 | 17,813 | 28,335 | 286,354 | 6% | |

| 10 | 286,354 | 17,181 | 28,335 | 275,200 | 6% | |

| 11 | 275,200 | 16,512 | 28,335 | 263,376 | 6% | |

| 12 | 263,376 | 15,803 | 28,335 | 250,844 | 6% | |

| 13 | 250,844 | 15,051 | 28,335 | 237,559 | 6% | |

| 14 | 237,559 | 14,254 | 28,335 | 223,478 | 6% | |

| 15 | 223,478 | 13,409 | 28,335 | 208,552 | 6% | |

| 16 | 208,552 | 10,428 | 27,009 | 191,971 | 5% | |

| 17 | 191,971 | 9,599 | 27,009 | 174,561 | 5% | |

| 18 | 174,561 | 8,728 | 27,009 | 156,281 | 5% | |

| 19 | 156,281 | 7,814 | 27,009 | 137,086 | 5% | |

| 20 | 137,086 | 6,854 | 27,009 | 116,932 | 5% | |

| 21 | 116,932 | 5,847 | 27,009 | 95,770 | 5% | |

| 22 | 95,770 | 4,789 | 27,009 | 73,551 | 5% | |

| 23 | 73,551 | 2,942 | 26,504 | 49,989 | 4% | |

| 24 | 49,989 | 2,000 | 26,504 | 25,485 | 4% | |

| 25 | 25,485 | 1,019 | 26,504 | - | 4% | |

| 297,019 | 672,019 | |||||

People encountering Islamic finance for the first time are often surprised that an interest rate can be referenced in the calculation of the rent that is to be paid. Shariah scholars permit this because the interest rate is merely being used to compute an amount; what gets paid is rent for occupation by the customer of the bank’s share of the property, not interest.

The financial implications are set out on Table D. The cash flows are identical to that of the variable rate repayment mortgage.

Unlike the murabaha mortgage, the diminishing musharaka poses no problems if the customer wishes to buy out the bank early. At any stage, the customer only needs to pay the amount shown on the table as the original cost of the part of the property owned by the bank.

This is achieved by giving the customer complete flexibility regarding when he buys out the bank, provided that he does so by the termination date of the contract.

There are three main issues.

The contracts used in Islamic finance need to avoid violating the requirements of Shariah (hence the term “Shariah compliant”) but there is no requirement for the governing law of the contracts to be Shariah. Islamic finance contracts made between a UK Islamic bank and a UK customer are always made under English law or Scottish law respectively.

Similarly Islamic finance contracts within the USA would normally be made under the law of the state where the property was located, e.g. Pennsylvania law.

Some countries give individuals a tax deduction for interest paid on a loan taken out to buy their private residence. Even though the UK no longer gives such a deduction, the UK does give a deduction for interest paid on a loan to purchase commercial premises or property purchased to rent to others.

For the diminishing musharaka contract, one would expect the rent paid by the customer to be deductible if loan interest would be deductible, but the tax law of the relevant country would need to be considered carefully.

However the murabaha contract presents greater problems. A tax system which looks at the economic substance of transactions will probably re-analyse the murabaha transaction as a financing transaction and concluded that it is equivalent to a loan at 5% interest.

However a tax system which looks primarily at the legal form of a contract will simply analyse the transaction as the Islamic bank selling the property to the customer for £790,182 as stated in the contract. That means there is no tax deductible finance cost.

In 2005 the UK brought in specific tax law which has the effect of re-analysing the murabaha transaction to classify the extra £290,182 paid by the customer as equivalent to interest for tax purposes. The tax law does not say that the £290,182 is interest; it merely treats it as being equivalent to interest for tax purposes.

Most countries have some kind of tax charged on the sale of real estate. In the UK the relevant tax is called Stamp Duty Land Tax (SDLT).

For a purchase financed with a conventional mortgage, the customer pays SDLT once on the third party price of £500,000.

However, with Islamic property finance, SDLT would be charged more than once. For example with the murabaha purchase the initial purchase price of £500,000 would be subject to SDLT and so would the sale by the bank to the customer for £790,182. This results in an overall SDLT cost much higher than with a conventional mortgage.

Similarly with the diminishing musharaka contract, the initial purchases of 25% for £125,000 and 75% for £375,000 would be subject to SDLT. SDLT would be payable again on £375,000 in stages over the 25 years as the customer buys out the bank’s 75% share of the property.

The UK legislated in 2003 to eliminate the extra SDLT charges, so that the Islamic property finance transaction bears the same SDLT cost as the equivalent conventional mortgage financed acquisition.

As explained above, the pricing for Islamic property finance is based upon prevailing market interest rates for conventional finance. That is inevitable in an economy where money can flow between the two sectors; having a price for “Islamic money” that was different from the price for “conventional money” would simply create arbitrage opportunities that would damage the Islamic finance sector.

In practice, Islamic property finance is usually more expensive than conventional property finance, even though both are based upon the same market price for money. There are two basic reasons for this:

As mentioned above, this paper is devoted entirely to Islamic property finance contracts that replicate conventional mortgage contracts. That is consistent with market practice, as the Islamic finance market mostly consists of replicating conventional contracts. It is possible to devise other Shariah compliant contracts that do not replicate conventional finance, but they form a small part of the market and are beyond the scope of this paper as they would unduly complicate it.

Follow @Mohammed_Amin