Serious writing for

serious readers

Refinancing in a Shariah compliant way can trigger any accrued taxable gain. At present UK tax law does not contain a relief for this transaction.

Summary

Posted 9 October 2019

The August 2019 issue of Tax Adviser (the house magazine of the Chartered Institute of Taxation "CIOT") had an article by me about a problem that is not well known, even amongst those who practice Islamic finance.

The article is reproduced below.

The purchase of real estate, whether a principal private residence or an investment property, is normally funded in part by equity provided by the purchaser, and in part by interest bearing debt provided by a bank or other financial institution.

However, many Muslims consider that Islam prohibits receiving or paying interest.

Accordingly, alternative acquisition structures have been developed which comply with the rules of Islam as interpreted by Shariah scholars, but which do not involve the payment of interest to the finance provider. Shariah scholars allow transactions to have similar economics to debt, provided they do not involve borrowing money or paying interest.

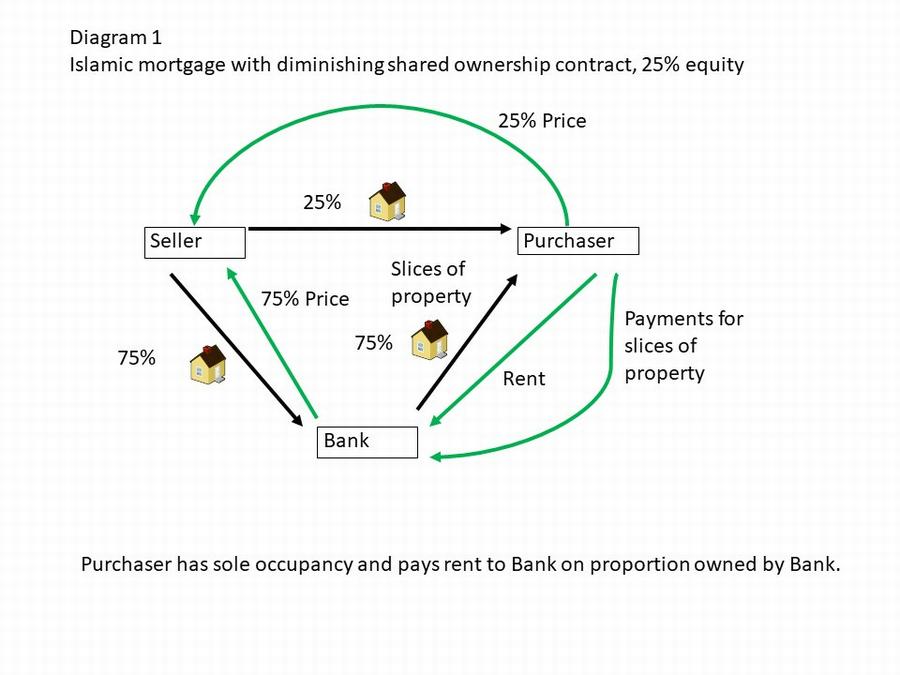

The most common structure used by Islamic banks in the UK is known in tax law (Income Tax Act "ITA" 2007 s564D and Corporation Tax Act "CTA" 2009 s504) as diminishing shared ownership.

It involves the purchaser and the bank buying the property jointly. The purchaser occupies the whole property, and pays rent to the bank on the bank’s share of the property. The rent can be fixed, but is more often re-set periodically, and in practice is set by reference to market interest rates plus the bank’s margin.

Over time, the purchaser gradually buys out the bank’s share of the property, (almost always at original cost) and as the purchaser does so, the level of rent falls as it is paid on a smaller proportion of the property.

The structure is illustrated in Diagram 1 with the equivalent of a 25% deposit.

Prior to specific legislation to enable it, this structure gave rise to several UK tax problems:

Changes in UK tax law have eliminated these problems. Finance Act "FA" 2003 s71A eliminates the double SDLT charge. ITA 2007 s564M and CTA 2009 s510 mean that for income tax purposes and corporation tax purposes the rent receives the same tax treatment as interest would receive.

Where property has little or no debt attaching to it, either because the debt has been paid down or because the property has appreciated in value, it is quite common for the owner to refinance it to take on more debt.

Private individuals do this to obtain money they can spend or give to family members, and real estate investors do this as part of the financial management of their real estate portfolio.

Taking on additional interest paying debt, even if it is secured on the property, involves no tax consequences. There are no SDLT transactions, and taking on extra debt secured on the property does not constitute a disposal of that property for capital gains tax purposes.

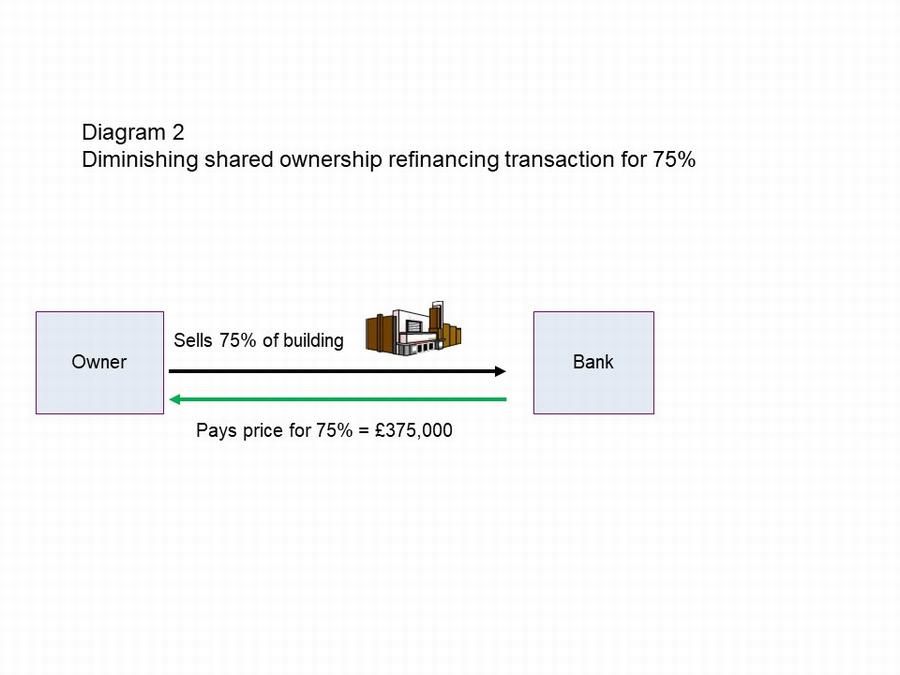

Muslims who consider that paying interest is religiously prohibited cannot, of course, refinance by taking out a loan secured on the property. However, the diminishing shared ownership structure can be used for refinancing purposes.

This is illustrated in Diagram 2. For simplicity, this assumes that the Owner before refinancing has attained 100% ownership of the property. The property is assumed to be worth £500,000 and the Islamic bank agrees to buy 75% of it for £375,000.

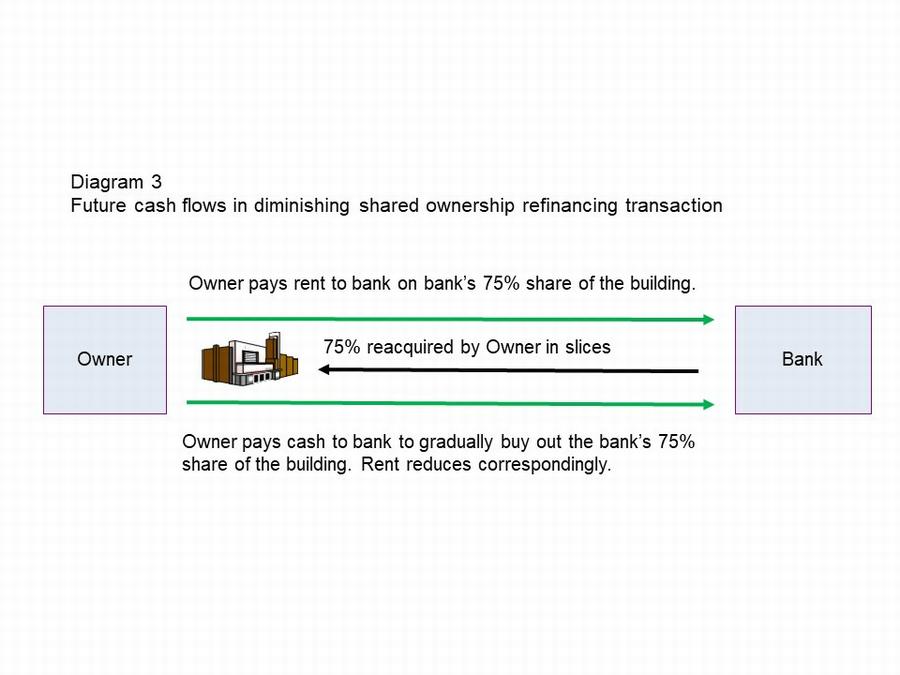

In future the Owner will pay rent to the bank, and will buy back the bank’s share of the property in slices, as illustrated in Diagram 3.

The SDLT reliefs cited above also apply to this transaction, so there should be no SDLT on either the sale of 75% by Owner to Bank, or its reacquisition. Also, the rent paid will receive the same tax treatment as interest would receive.

However, the sale by Owner to Bank of 75% of the property is a part disposal of the property for capital gains tax "CGT" purposes. There are no specific relieving provisions.

If the property is the Owner’s principal private residence, the part disposal will not give rise to any CGT liability. Otherwise however it is a taxable disposal. If the building now worth, say £500,000 and cost £100,000, then the taxable gain is £300,000 computed using the part disposal formula.

Perhaps because Islamic finance is a relatively niche subject, there is a surprising lack of awareness of this exposure amongst professionals serving clients who might engage in Islamic financing of real estate transactions.

In my view, eliminating this tax exposure would require primary legislation. While the Treasury has power (now contained in Taxation (International and Other Provisions) Act 2010 s366) to vary the alternative finance arrangements provisions by regulation, in my opinion that power is not broad enough to enable a regulation to specify that the sale to the bank for refinancing purposes is not a disposal.

However drafting innovation is not required, because there is existing statutory language which could readily be re-purposed.

This relates to the tax law (ITA 2007 s564G and CTA 2009 s507) for investment bond arrangements. This exists to facilitate an Islamic finance structure called sukuk in Arabic. The structure normally entails an Owner selling real estate to a Special Purpose Vehicle “SPV” which pays for it by issuing investment bonds. The Owner then pays rent to the SPV and eventually buys back the real estate.

As well as the basic law for investment bonds cited above, there are further provisions in FA 2009 Schedule 61 para 5. In brief, they require (using the terminology of the transaction above)

Provided these conditions are satisfied, then for CGT purposes each of the sale of the building by the owner to SPV, the lease from SPV to the owner, and the sale of the building by SPV back to the owner are not treated as disposals.

The CIOT has raised this problem with HM Revenue & Customs, and suggested equivalent legislation to FA 2009 Schedule 61 para 5 should apply where part or all of building is sold, and then re-acquired using diminishing shared ownership. However, the Government has currently declined to legislate, giving the response below with authorisation to publish it:

“The government recognises the need for greater stability in the tax system and as such, recognises the importance of an evidence based approach to policy changes. To date, evidence of the scale of the issue has been limited making justification of a change in legislation challenging. All tax policy is kept under review and any new evidence as to the extent to which the existing legislation is affecting market outcomes will be considered carefully as part of that process.’’

Accordingly advisers need to be aware of the problem to avoid their clients stumbling into this CGT trap, and to point out the correct reporting obligations if a disposal has already been triggered.

I originally wrote about this problem in my 20 May 2018 website page "UK taxation needs to accommodate Shariah compliant real estate refinancing" which was based on an article I wrote in the magazine "Islamic Finance News."

That article was less technical than the one above. The reason is that Islamic Finance News has an international readership of Islamic finance practitioners, only a few of whom specialise in taxation. Conversely "Tax Adviser" magazine is aimed at UK tax specialists.

Follow @Mohammed_Amin