Serious writing for

serious readers

In my view, a transaction between two wholly owned companies is a nullity for religious purposes, so no religious prohibitions can apply.

Posted 7 July 2019

A question about something which is obvious is often difficult to answer definitively. Its very obviousness means that few are likely to have written about it before.

My June 2019 column in the magazine "Islamic Finance News" addressed one such question. You can read it below.

An email came via my website from someone who is writing a doctoral thesis on the taxation of multinationals in the MENA region. He mentioned my website article “Islamic and conventional banks face almost identical transfer pricing issues” and had two questions:

On corporations, I explained that although traditional Islamic law (fiqh) never invented them, every Muslim majority state I know about has legislation for corporations. The religious permissibility of corporations is clearly accepted by the scholars who set Shariah standards such as the AAOIFI Shariah Board.

The second question was more challenging. Before addressing it, to help non-tax specialists I will explain the background.

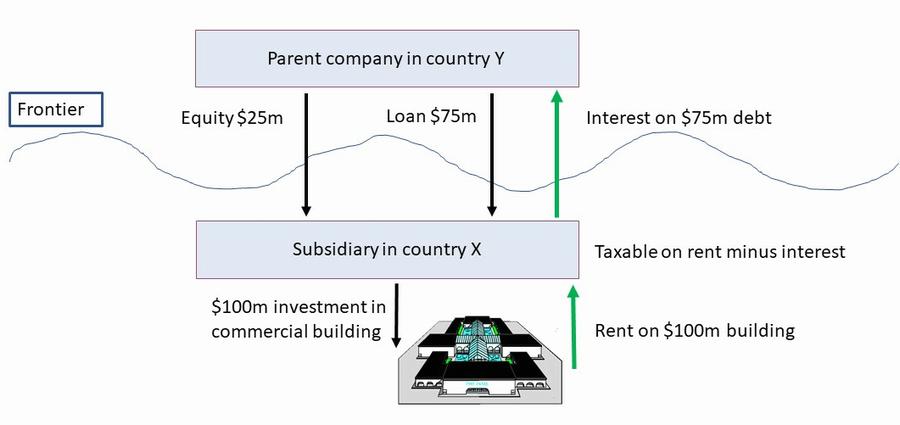

Within wholly owned multinational groups it is often desirable for tax planning purposes to have interest-bearing loans between companies.

For example, assume that Country X charges corporation tax of 25% on rental income, but allows a deduction for interest paid, and has a zero withholding rate on interest paid from Country X to Country Y.

If a Country Y company purchases a Country X investment property using $100 million of its own funds, it will suffer 25% Country X corporation tax on the rental income.

Alternatively, the Country Y company could set up a wholly owned subsidiary in Country X and capitalise it with $25 million of share capital. The Country Y parent then makes a $75 million interest-bearing loan to the Country X subsidiary which then has $100 million to buy the investment property. Now Country X corporation tax will be significantly lower because interest on the $75 million loan is deductible from the rental income before computing the Country X subsidiary’s corporation tax liability.

I was not aware of any fatwas from organisations such as AAOIFI on this subject. However, I would not expect any. The Shariah standards are all about transactions with third parties rather than purely internal transactions. A subsequent review of the AAOIFI Shariah standards has not found anything.

However, in my professional practice before I retired, I regularly came across such loans set up in private transactions by investors who wished to be Shariah compliant, approved by their Shariah advisers.

The religious analysis here is relatively straightforward.

If you own 100% of a company, it is entirely your creature (apart from local legal requirements.) Accordingly, if you cannot do something religiously, such as running a casino, neither can a company which you wholly own.

The same logic says that from a religious perspective any transaction between you and your 100% owned company does not exist. (The transaction does exist for state law since the company has legal personality.)

Conceptually, it is no different from keeping tin of money for buying food and another tin of money to pay for utilities. If you “borrow” $10 from the utility tin and add it to the food tin, and later “repay” $11 from the food tin to the utility tin as compensation, nobody would ever complain that you had paid $1 interest between the two tins. They are both 100% yours.

The companies look more complicated, but if 100% owned, the religious logic is the same.

Follow @Mohammed_Amin