Serious writing for

serious readers

Summary

3 May 2014

In December 2013 I was asked to contribute a section for the "Global Islamic Finance Report 2014" (GIFR)which is published by Edbiz Consulting with Professor Humayon Dar as Editor-in-Chief. See their website www.gifr.net

I decided to write about the tax policy challenges facing governments of the advanced economies which are members of the Organisation for Economic Cooperation and Development (OECD). Many governments are concerned about the loss of corporate tax revenue as business becomes increasingly mobile, assisted by technological developments such as the internet. In my view there is a risk that policy responses these tax challenges could, inadvertently, impact adversely upon the taxation of Islamic finance transactions. However with appropriate policy design, it should be possible to avoid such adverse outcomes.

The GIFR 2014has now been published. My contribution appears as the Part 2 of "Chapter 12 - Taxation". Now that the GIFR 2014 has been published, I am making my own writing available below, exactly as I submitted it. (There were immaterial changes made by the editor of the GIFR which is normal in publishing.)

This chapter looks at some of the tax policy challenges facing OECD governments in the context of international business. It then considers how these can impact upon the taxation of international Islamic finance transactions and makes some recommendations regarding the way forward.

The fundamental concepts that apply to the taxation of international business were developed during the latter part of the 19th century and the first years of the 20th century. The business environment was very different at that time.

Communications were very slow. Although a small amount of communication could take place at high speed using telegraph cables, there was very limited bandwidth to use modern vocabulary. Accordingly it was only practical use telegraph for short high importance communications. Travel between distant locations on land relied upon railways with journey times measured in days or weeks while long-distance sea travel was slower still.

Despite the slowness of the communications and travel, international trade and international business did exist and grew steadily. There were two basic trading models.

Consider a UK manufacturer who has found a customer in Malaysia. (It is easier to write using specific country names. However any reference to Malaysia in the 19th century is strictly an anachronism. Furthermore, except where explicitly stated, none of the discussion which follows is specific to the UK or Malaysian tax system.) The customer relationship may have been established by the UK manufacturer sending a salesman to Malaysia or by the Malaysian enterprise sending someone to the UK to find appropriate suppliers.

The UK manufacturer having agreed a quantity and price with the Malaysian customer will ship the goods to Malaysia. The manufacturer may require payment up-front, or may require the Malaysian customer to secure payment (for example by a letter of credit accepted by a UK bank) or may be willing to accept taking on the Malaysian customer's credit risk. Questions regarding payment arrangements are not considered further in this chapter and have no impact upon the tax treatment. Quite often the goods will be shipped by using a third-party carrier; ownership in the goods may pass when the UK firm delivers them to the shipping agent or may remain with the UK firm until the shipping agent delivers the goods in Malaysia.

The UK government will clearly wish to tax the UK manufacturer on any profits made as the manufacturer is resident in the UK and carrying out manufacturing there.

The question is whether Malaysia can tax the UK manufacturer on the profits made from selling the goods to the Malaysian customer. Some countries may wish to tax this profit, particularly if the contract for the sale of the goods is negotiated and made within Malaysia by the UK firm's salesman who has travelled there to negotiate the sale.

Over time the international convention has developed that a country in the Malaysian circumstances described above does not seek to tax the UK manufacturer on the grounds that the UK manufacturer does not have a sufficient connection with Malaysia, even if a travelling salesman negotiates and agrees the contract. In some cases this may be made clear by domestic law but in most cases one relies upon double taxation treaties agreed between the countries. Under such a treaty the norm would be that the UK manufacturer would not be taxable in Malaysia unless the manufacturer had a "permanent establishment" there as discussed below.

As an alternative, and particularly if the Malaysian market is likely to be important on a continuing basis, the UK manufacturer may set up a branch in Malaysia. This would be likely to involve owning or renting premises where a stock of goods would be maintained. The UK manufacturer would probably send some UK employees to be based in Malaysia at the premises, as well as recruiting some local Malaysian staff. The Malaysian branch would be expected to find customers, make sale contracts and provide after sales service.

The goods would continue to be manufactured in the UK but the manufacturer would ship appropriate quantities to the Malaysian branch where they would be stored until the Malaysian branch found customers and made sales.

In these circumstances the UK manufacturer clearly has a substantial and continuing connection with Malaysia through its branch. In international tax language, such a branch is referred to as a "permanent establishment."

It is an accepted norm of international taxation that the country where the branch is located, here Malaysia, can tax the profits made by the branch. The branch can prepare accounts reporting its sales, deducting its local costs and deducting something for the cost of the goods that the branch obtains from its “head office” which is the UK manufacturer. The norm for tax purposes is to treat the branch as acquiring the goods at the same price that would be paid by a third party purchaser in the same circumstances, irrespective of how the manufacturer and the branch actually account for the transfer of the goods from the UK to Malaysia.

There are two alternative ways for the home country, here the UK, to take account of the Malaysian tax being paid by the UK manufacturer’s branch in Malaysia.

As well as trade in goods, the latter part of the 19th century also saw a growing level of international investment in real estate, shares and loans. Such activities also give rise to international tax questions:

Again, it has become the norm for countries to address such questions when negotiating double taxation treaties. The UK/Malaysia treaty will specify whether Malaysia can tax the items mentioned above; if Malaysia can tax, the treaty may specify the maximum rate of tax that can apply. Such tax is often referred to as withholding tax since typically the country from which the payment is made will require the payer to deduct the tax when making the payment and remit that tax to the tax authorities; this avoids the need for the tax authorities to require the foreign recipient to file a tax return, particularly since there are limited enforcement mechanisms available where the recipient is overseas.

Unlike the late 19th century, international communications are now very cheap and essentially instantaneous with no meaningful limits on bandwidth. Travel between far distant countries is rapid and relatively cheap using jet aeroplanes.

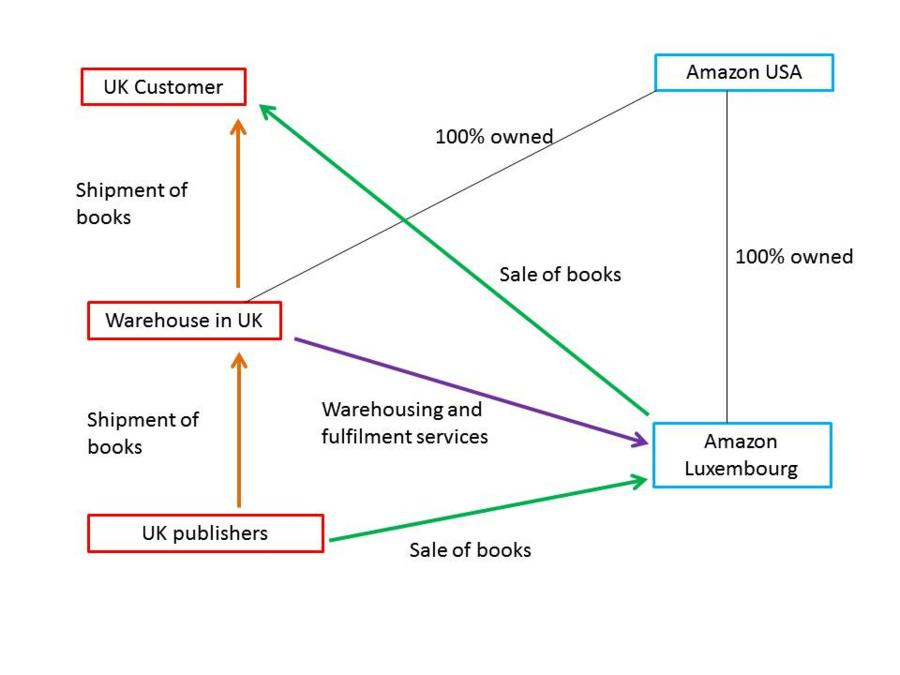

This is leading to the above categorisation system breaking down. Consider how Amazon.com sells books in the UK as illustrated in the diagram below. (The writer previously advised many multinational companies and therefore wishes to make it clear that the following comments are based entirely on public domain information.)

In this simplified illustration, the parent company Amazon USA has two subsidiaries, one in the UK that owns and operates a warehouse and one in Luxembourg that carries on a business of selling books. Amazon Luxembourg purchases books in bulk from UK publishers. The publishers are instructed to ship the books to the UK warehouse where they are stored. However the ownership risk in the books rests with Amazon Luxembourg which will suffer the loss if the books cannot be sold at appropriate prices.

When a UK customer uses the website www.Amazon.co.uk to purchase a book, the contract is actually made with Amazon Luxembourg which receives payment from the UK customer via his credit or debit card. Amazon Luxembourg will instruct the UK warehouse to ship the book to the UK customer.

The UK warehouse never owns any books and takes no business risk in respect of the books. All it does is to charge Amazon Luxembourg for warehousing and fulfilment services, making a relatively small profit which is taxable in the UK. Amazon Luxembourg makes profits from the sale of books, assuming that they can be sold for more than cost. That profit is made in Luxembourg where Amazon Luxembourg is based and not in the UK as Amazon Luxembourg does not have any place of business in the UK. The Luxembourg tax on the bookselling profits is much lower than would be the tax paid if the business were carried on in the UK.

For simplicity the US tax treatment of the foreign subsidiaries is ignored. However there are various complex mechanisms which ensure that the USA does not tax either Amazon Luxembourg or the UK warehousing company.

Somewhat similarly, Google has a significant workforce in the UK whose responsibility is to help UK advertisers make the best decisions regarding the kind of advertising services they wish to purchase from Google. However all of Google's advertising services in the UK are sold and delivered electronically from Google Ireland so the advertising services are taxable in Ireland and not in the UK.

Issues such as those described above are causing OECD countries to reconsider how international business should be taxed. On 19 July 2013 the OECD published its "Action Plan on Base Erosion and Profit Shifting" which discusses in more detail the kind of issues outlined above and proposes how tax authorities might address them.

Islamic finance is the provision of finance within the rules of Shariah as specified by the Islamic finance scholars who advise the Islamic financial institutions and other Muslim counterparties involved. Typically Islamic finance involves carrying out transactions in real assets to achieve the same economic consequences that would be achieved in conventional finance by making interest-bearing loans.

Two specific examples are considered below.

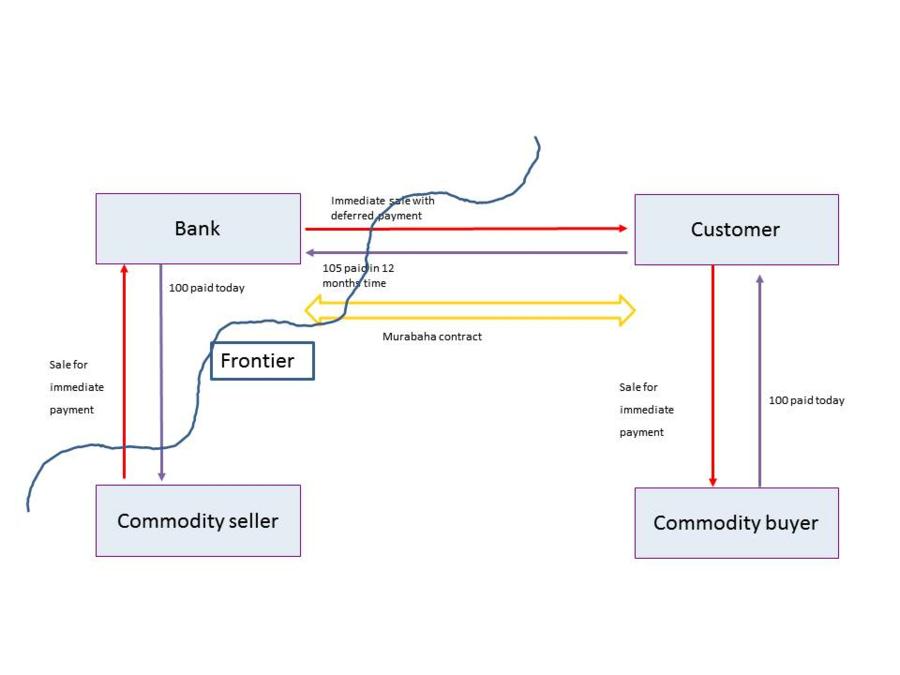

In this example a foreign bank enters into a commodity murabaha transaction to provide short-term finance to a customer within the country under consideration. The transaction can be illustrated as follows:

Here the foreign bank purchases a commodity such as refined copper from a seller located within the country and sells the commodity to a customer located within the country. It is quite likely that the bank may have some agents located within the country that organise and facilitate these transactions rather than carrying them out entirely remotely. The customer is then responsible for selling the commodity to obtain cash. In practice the bank may help to facilitate that by introducing the commodity buyer to the customer and may even act as the customer's agent in carrying out that sale. The precise details of how much the bank can assist the customer in selling the commodity will depend upon the advice of the Shariah scholars.

When persons based in a country regularly carry out purchase and sale transactions on behalf of a foreigner (the bank) they may cause the foreign bank to have a permanent establishment within the country. This is a complex area of tax law but the risk of a permanent establishment is a very real one. The consequence would be that the bank’s profit from the purchase and resale transaction would be subject to tax within the country at the full rates of tax applicable to business profits.

In comparison, the international norm is that interest paid by a person such as the customer to a foreign bank would either not be taxable at all by the country where the customer is located or would be subject only to withholding tax at a rate significantly lower than the full rate of tax applied to business profits.

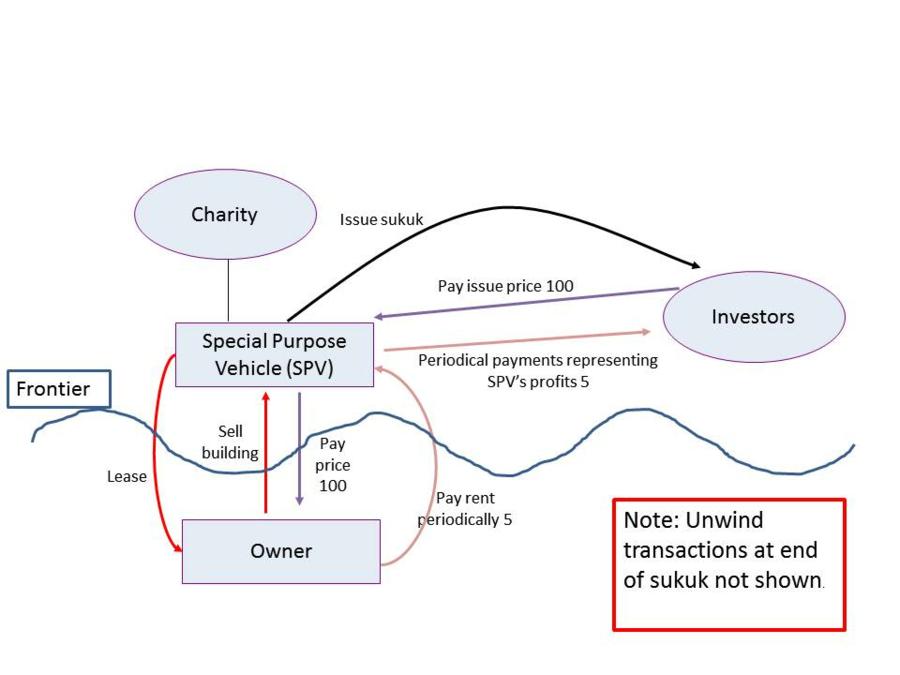

As this transaction is relatively complex, it is worthwhile describing the precise steps involved.

The steps involved in creating, operating and unwinding this structure give rise to a number of tax questions. These include the following:

If these tax costs do arise, they are likely to make the sukuk transaction prohibitively expensive and unworkable. As a comparison, no such taxes would be expected to arise if Owner had issued a conventional bond to the investors, with the possible exception of withholding tax on interest paid to the investors. However even in the case of withholding tax, it is sometimes the case that rental income suffers a higher rate of withholding tax than interest income. The opposite rarely occurs.

OECD governments are under great fiscal pressure as a result of the aftermath of the global financial crisis. This has been aggravated by the scope for internationally mobile businesses to fragment their activities between countries to reduce their taxes payable, taking advantage of the ease of modern communications and travel.

Governments are likely to respond to the challenges discussed above by increasing the number of circumstances in which a foreign person having some kind of activity within the jurisdiction is treated as having a taxable presence. This would mean modifying the existing definitions of a "permanent establishment" within international tax treaties so that more kind of activity would constitute a permanent establishment. There may also be an increased desire to charge withholding taxes on payments being made to foreign persons.

Such measures if enacted are likely to cause collateral damage to the Islamic finance industry by increasing the likelihood of taxation on Islamic finance transactions, where such taxation would not arise on a conventional finance transaction. For example, in the case of the commodity murabaha transaction mentioned above, any moves to tighten the definition of a permanent establishment are likely to increase the risk that the foreign bank is found to have a permanent establishment in the country where the murabaha transactions are taking place. This would cause the foreign bank to suffer tax in that country whereas the making of a conventional loan may well be exempted from tax. Similarly, the transactions involved in the sukuk arrangements are likely to face higher taxation than the issue of a conventional bond.

OECD governments need to enact specific legislation to avoid creating an additional tax burden on Islamic finance transactions. As mentioned above, this additional tax burden might arise either under the existing tax law (which will have been developed in a purely conventional finance environment) or under any revisions to tax law made as part of countering base erosion and profit shifting.

The OECD presently has 30 member countries. Of these, only Turkey has a Muslim majority. The other 29 will be reluctant to legislate specifically for Islamic finance as most will have a strong tradition of separating church and state and will not wish to base tax rules upon religious principles. However the United Kingdom has shown that it is possible to create tax rules which enable Islamic finance transactions to receive a tax treatment equivalent to that accorded to conventional finance without bringing religion into tax law.

The approach that the United Kingdom has taken is to define particular types of transactions and then specify their tax treatment. The transactions are not defined by reference to Islamic finance but are of a type that Islamic financiers are likely to use. This is best explained by the specific example of a purchase and resale transaction as defined in UK tax law.

(1) This section applies to arrangements if—

(a) they are entered into between two persons (“the first purchaser” and “the second purchaser”), one or both of whom are financial institutions, and

(b) under the arrangements—

(i) the first purchaser purchases an asset and sells it to the second purchaser,

(ii) the sale occurs immediately after the purchase or [deleted for brevity]

(iii) [Deleted for brevity]

(iv) the second purchase price exceeds the first purchase price, and

(v) the excess equates, in substance, to the return on an investment of money at interest.

(2) [Deleted for brevity]

(3) In this section—

“the first purchase price” means the amount paid by the first purchaser in respect of the purchase, and

“the second purchase price” means the amount payable by the second purchaser in respect of the sale.

(4) [Deleted for brevity]

Corporation Tax Act 2009 section 503 is reproduced in the sidebox, slightly abridged by deleting for brevity parts that are not relevant.

It is quite clear that this legislation is describing a transaction equivalent to a murabaha transaction, but there is no reference to Islamic finance or usage of Arabic terms. Other parts of the tax legislation (not reproduced here) have the effect of treating the difference between the first purchase price and the second purchase price in the same way that a payment of interest made by the second purchaser to the first purchaser would be treated.

Similarly, Corporation Tax Act 2009 section 507 (not reproduced for brevity) defines an "Investment Bond" transaction which when read carefully will be seen to be the issue of a sukuk. Other parts of the tax law then give rise to a number of favourable tax consequences provided that it is clear when the initial sale of the building takes place that it will be reacquired by the original owner within 10 years. In particular:

Other OECD governments are recommended to amend their tax law using the same strategy as that adopted by the United Kingdom in order to facilitate Islamic finance transactions while not privileging Islamic finance above conventional finance.

It is quite critical that in all parts of the UK tax legislation which defined transactions which are likely to be used by Islamic financiers, the description specifically requires the economic return is involved to equate "in substance, to the return on an investment of money at interest." This is intended to ensure that the tax law can only apply to transactions that are equivalent to interest-bearing debt.

Islamic financiers often complain that the tax rules should be extended to other forms of Islamic finance transaction which are equivalent to equity investment. If the UK were to do so, Islamic finance structures could be used to reduce UK taxes in ways that could not be achieved using conventional finance structures. This would be entirely contrary to a tax policy which seeks to counter "Base Erosion and Profit Shifting."

Follow @Mohammed_Amin