Serious writing for

serious readers

Summary

Posted 12 December 2010

The text below was written in June 2008 to form a chapter in the book "Euromoney Encyclopedia of Islamic Finance" edited by Aly Khorshid and published by Euromoney Books.

My chapter is reproduced here with the consent of the publishers. My goal in writing it was to explain the different approaches to the taxation of Islamic finance taken by the UK and some Muslim majority countries.

The tax treatment of a transaction is a fundamental part of any evaluation of its economics. Tax law however differs from country to country.

Accordingly, this chapter considers two specific Islamic finance structures to assess how they might be treated for tax purposes in different countries. After a brief review of the tax position, it then considers what general conclusions can be drawn.

For simplicity, this chapter considers:

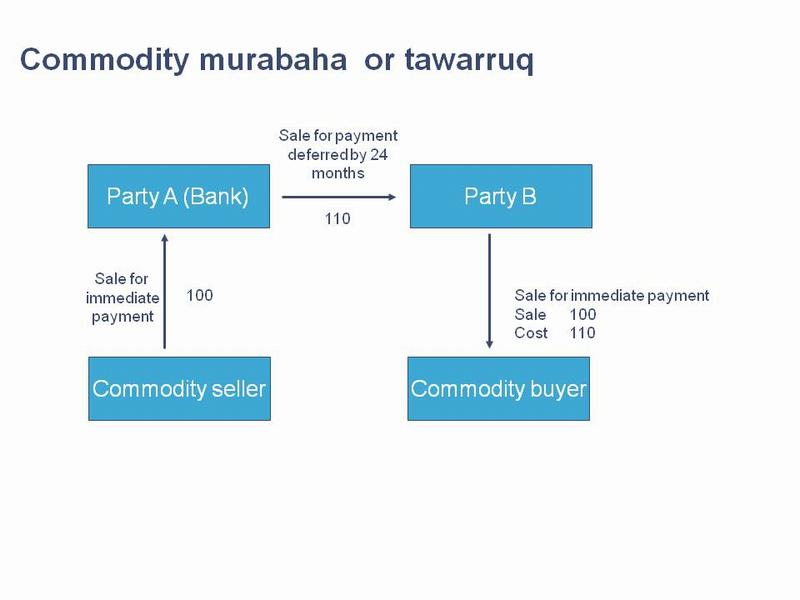

This transaction is used when Party A wishes to advance money to Party B. It can be illustrated with the following diagram:

Diagram of a commodity murabaha or tawarruq transaction

Party A (usually a bank) will buy something that can be sold very easily afterwards and with little difference between the bid/offer (buy/sell) prices. A typical example would be a quantity of copper bought in a commodity market. Party A buys the copper, immediately paying £100 for it, and transfers ownership to Party B at a price of £110 payable in, say, two years time.

Party B can then immediately sell the copper for a price of about £100. This gives Party B cash equal to what Party A has laid out, £100, and an obligation to pay Party A £110 in two years time. The extra £10 is the cost of the finance, and corresponds to a simple interest rate of 5% pa.

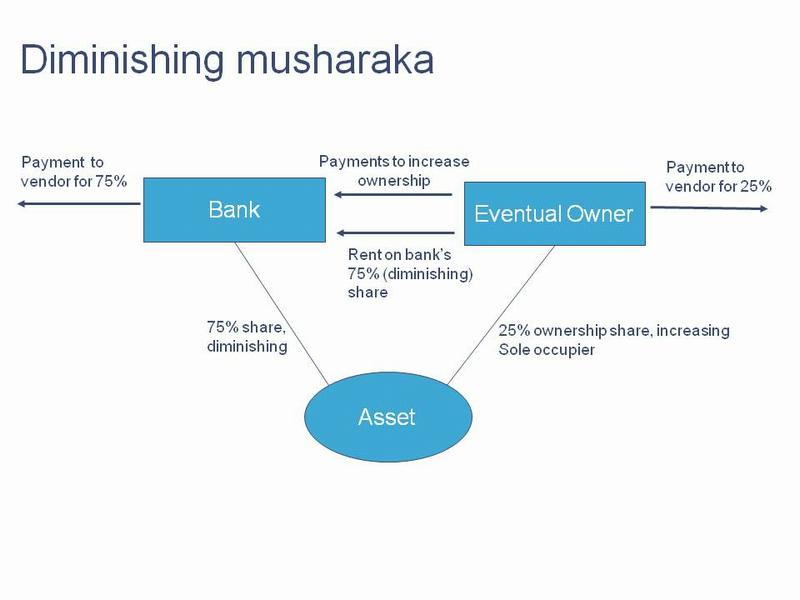

This is often used by people buying houses for owner occupation instead of a conventional mortgage, but can also be used for the purchase of investment property. It is illustrated in the following diagram.

Diagram of a diminishing musharaka transaction

Diminishing musharaka is used when one party, here called the ‘eventual owner’, wants to buy an asset but cannot afford to pay for all of it. In the diagram, on day one the bank buys 75% of the asset, for example a building, while the eventual owner buys 25%. Under the contract the eventual owner has immediate rights to sole occupation of the entire building.

The eventual owner pays rent to the bank on the 75% of the property that he doesn’t own. Then, over the life of the arrangement, as well as paying the rent, the eventual owner will make additional payments to the bank to purchase additional slices of the asset. These purchases may be at the option of the eventual owner, although usually the bank will also have a ‘put’ option to require the property to be purchased at some stage.

The key question in the tax treatment of the tawarruq transaction is whether the finance cost which is implicit in Party B’s deferred purchase price of £110 and immediate sale price of £100 is recognised as such for tax purposes.

Many Muslim majority countries where Islamic finance is practiced do not have a corporate income tax, as it is not needed due to the level of government revenues from natural resources. However, others that do such as Egypt treat the £10 difference as a finance cost without considering specific legislation to be needed. As the legal systems of Muslim majority countries have been heavily influenced by, or are expressly based on, Shariah, one would expect a Shariah compliant financial transaction to have its implicit finance cost recognised as such for tax purposes.

Malaysia however has put the matter beyond doubt. Section 2(7) of the Malaysian Income Tax Act 1967 provides that:

“Any reference in this Act to interest shall apply, mutatis mutandis, to gains or profits received and expenses incurred, in lieu of interest, in transactions conducted in accordance with the principles of Shariah.”

This means that the Malaysian income tax legislation treats ‘profits’ to be similar to interest making the taxability or deductibility of ‘profits’ similar to the treatment of interest in a conventional financing agreement. All of the other requirements of Malaysian tax law governing when interest is taxable or deductible are then applicable.

In the case of Western countries where Shariah compliant transactions are still relatively new, there is no reason to assume that any particular tax treatment will apply.

One of the factors that distinguish tax systems from one another is the relative emphasis they each place on “form” and “substance.” In this context, “form” is used to describe putting significant emphasis upon the legal form of a transaction, in other words how is the transaction implemented from a legal perspective? In contrast, “substance” is used to denote an approach of basing the tax treatment primarily upon the economic reality of a transaction. Tax systems based entirely on “form” or entirely on “substance” do not exist. Instead, there is a spectrum, with countries combining the two elements in varying degrees. Furthermore, different parts of a country’s tax system may have distinct positions on the spectrum.

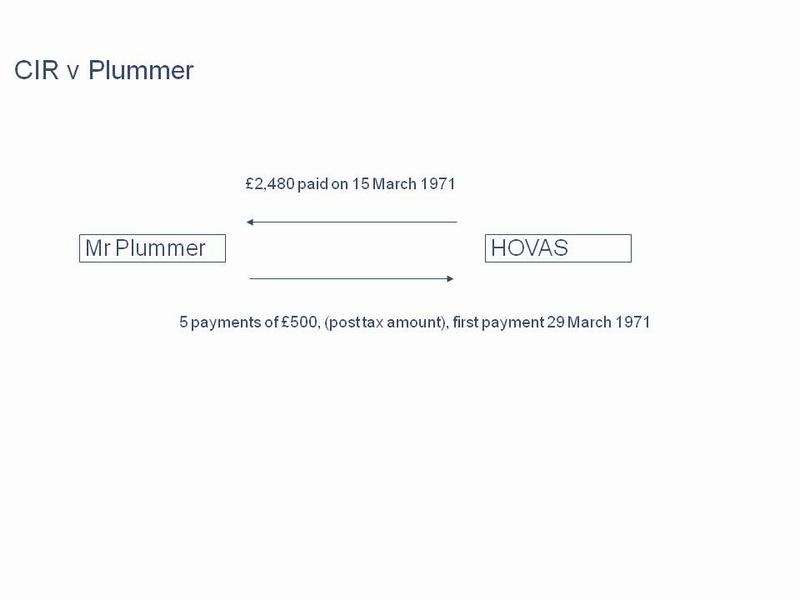

To illustrate the distinction between form and substance, it is helpful to review a UK tax case, Commissioners of Inland Revenue (CIR) V. Plummer, citation 54 Tax Cases 1. While the case was heard several decades ago, and its specific facts have been superseded by subsequent changes in UK tax law, it illustrates the form and substance distinction very clearly.

Diagram of the UK tax case "CIR v Plummer"

The facts of the case are relatively simple. On 15 March 1971 a charity called HOVAS paid £2,480 to Mr Plummer. In exchange, he undertook to make five annual payments to HOVAS under a deed of covenant, with the first payment due on 29 March 1971. The amount of each annual payment was whatever sum, after deduction of all taxes, amounted to £500.

The substance of the transaction was that Mr Plummer was borrowing £2,480 from HOVAS and repaying this in five annual instalments of £500; effectively borrowing at a relatively small rate of interest.

Under the legal form adopted, each of the £500 payments was treated as a larger gross payment from which Mr Plummer was entitled to withhold and retain income tax at the standard rate. For example, at the tax rate then prevailing, the first payment was legally a gross payment of £851.06. As a charity, HOVAS was entitled to a refund from the Inland Revenue of the tax withheld of £351.06, making the transaction very attractive to HOVAS; an internal rate of return of 27% was mentioned during the litigation.

Under the tax law then prevailing, Mr Plummer was entitled to offset the gross payment of £851.06 when computing his liability to higher rate tax, but not standard rate tax. (The standard rate tax relief was already achieved by him deducting and retaining the £351.06.) Accordingly, the transaction was also extremely attractive to Mr Plummer as a way of reducing his higher rate tax liability.

The tax authorities litigated and the case went through every level of the UK court system. Mr Plummer was successful before the Special Commissioners, before the High Court in 1977, before the Court of Appeal in 1978 (where the judges decided 3-0 in his favour) and before the House of Lords in 1979 (where the judges decided 3-2 in his favour).

The case is instructive to read as the legal arguments were directed almost entirely to the legal form of the transactions and whether the detailed stipulations of UK tax law had been complied with. The Inland Revenue did not attempt to argue that the transaction should simply be taxed on its economic substance as such an argument would find no support in UK tax law. (The courts might well take a different approach today, given the way case law has subsequently evolved in the UK.)

Against this background, tax systems which seek to identify the “substance” (i.e. the underlying economics) of the transaction have no difficulty deciding that Party B has suffered a £10 finance cost. Quite clearly the only reason Party B is paying £110 for copper that it can only resell for an immediate payment of £100 is that Party B is granted a two year deferral before it needs to pay the £110. This treatment applies in the Netherlands and in the USA, both tax systems which look very much to the substance of a transaction.

Conversely, the UK approach is that the tax treatment is heavily influenced by the legal form of the transaction. The legal form is that Party B has actually purchased an amount of copper at a price of £110 and then sold that copper, for immediate payment, at a price of £100. Accordingly, its loss has arisen on the purchase and resale of copper.

Such a loss on the purchase and resale of a commodity may not be tax deductible. In the UK, for example, unless Party B can show that it is trading (as understood by tax law) in copper, it will not be entitled to deduct the £10 loss against its other income. Furthermore, even if Party B regularly trades in copper, this transaction does not look like a legitimate trading transaction since Party B knew that it would suffer a £10 loss when it commenced the transaction. (Trading is normally done with a view to profit.) Accordingly, under UK tax law (before the recent changes to facilitate Islamic finance discussed below), Party B would not be expected to obtain tax relief for its £10 cost.

The UK is a pioneer amongst Western countries in adapting its tax system to facilitate Islamic finance. Accordingly, the strategic considerations that underlie the UK approach merit analysis, as the UK’s example may be followed by other Western countries that seek to encourage Islamic finance.

The tax law changes governing the computation of taxable income were introduced by the Finance Act (FA) 2005, with subsequent expansion of the range of transactions covered in FA 2006 and FA 2007. A review of the legislation enables one to ‘reverse engineer’ the design considerations that underlie it. Four key principles emerge:

Strictly speaking, the UK has not enacted any Islamic finance legislation. A search of FA 2005 will fail to find words such as Islamic, Shariah, tawarruq or any other term used specifically in Islamic finance. The reason is that the tax treatment of a transaction cannot be allowed to depend upon whether it is Shariah compliant. As well as introducing significant uncertainty into the UK tax system, introducing Shariah considerations would create a situation where all taxpayers were not receiving identical tax treatment.

Instead, the UK identified certain types of transaction widely used in Islamic finance, and ensured that those types of transaction received appropriate tax treatment. This is illustrated by FA 2005 section 47 “Alternative finance arrangements”, reproduced here in full as originally legislated:

(1) Subject to subsection (3) and section 52, arrangements fall within this section if they are arrangements entered into between two persons under which—

(a) a person (“X”) purchases an asset and sells it, either immediately or in circumstances in which the conditions in subsection (2) are met, to the other person (“Y”),

(b) the amount payable by Y in respect of the sale (“the sale price”) is greater than the amount paid by X in respect of the purchase (“the purchase price”),

(c) all or part of the sale price is not required to be paid until a date later than that of the sale, and

(d) the difference between the sale price and the purchase price equates, in substance, to the return on an investment of money at interest.

(2) The conditions referred to in subsection (1)(a) are—

(a) that X is a financial institution, and

(b) that the asset referred to in that provision was purchased by X for the purpose of entering into arrangements falling within this section.

(3) Arrangements do not fall within this section unless at least one of the parties is a financial institution.

(4) For the purposes of this section “the effective return” is so much of the sale price as exceeds the purchase price.

(5) In this Chapter references to “alternative finance return” are to be read in accordance with subsections (6) and (7).

(6) If under arrangements falling within this section the whole of the sale price is paid on one day, that sale price is to be taken to include alternative finance return equal to the effective return.

(7) If under arrangements falling within this section the sale price is paid by installments, each instalment is to be taken to include alternative finance return equal to the appropriate amount.

(8) The appropriate amount, in relation to any instalment, is an amount equal to the interest that would have been included in the instalment if—

(a) the effective return were the total interest payable on a loan by X to Y of an amount equal to the purchase price,

(b) the instalment were a part repayment of the principal with interest, and

(c) the loan were made on arm’s length terms and accounted for under generally accepted accounting practice.

Reading section 47, it is clear that it was designed to facilitate murabaha and tawarruq transactions. However it nowhere uses those terms and nothing in section 47 limits its application to Islamic finance. If a transaction falls within section 47, the tax treatment follows automatically, regardless of whether the transaction is (or was intended to be) Shariah compliant.

Commercial sales of goods often involve a credit period for the customer. It would unduly complicate UK tax law if every sale of goods with deferred payment required identification of the price that would have prevailed if no credit were given, and then giving separate tax treatment for the implied cost of the credit. Consider for example a food manufacturer selling hundreds of thousands of tins of food to retailers with 30 days credit allowed for the payment of each sales invoice.

Section 47 limits its impact by requiring the involvement of a financial institution in subsection (3). This ensures that only transactions where finance is provided by or to a financial institution fall within the new rules. Accordingly, the food manufacturer and its customers should not be impacted by these new rules. (One drawback of this approach is that it is currently impossible for two non-financial companies to transact Islamic finance with each other and receive the tax treatment given by the new legislation.)

Financial institution is defined in section 46(2) as:

(2) In this Chapter “financial institution” means—

(a) a bank as defined by section 840A of ICTA [1988],

(b) a building society within the meaning of the Building Societies Act 1986 (c. 53),

(c) a wholly-owned subsidiary of a bank within paragraph (a) or a building society within paragraph (b),

(d) a person authorised by a licence under Part 3 of the Consumer Credit Act 1974 (c. 39) to carry on a consumer credit business or consumer hire business within the meaning of that Act, or

(e) a person authorised in a jurisdiction outside the United Kingdom to receive deposits or other repayable funds from the public and to grant credits for its own account.

Tracing through the definitions establishes that they cover all banks licensed in the European Economic Area and also persons licensed to take deposits in other countries, which is the key practical definition of a bank. However many other bodies engaged in financial activities, such as hedge funds, fall outside these definitions.

Section 47 reproduced above demonstrates how complex it can be to legislate for an apparently straightforward transaction. Drafting the new legislation would have been very arduous if it was then necessary to legislate specifically for all the tax consequences flowing from murabaha or tawarruq transactions.

The legislation avoids this burden by assimilating the tax consequences of Islamic finance transactions into the existing tax legislation. For example, where a company undertakes a murabaha or tawarruq transaction, the tax consequences are governed by FA 2005 section 50 (1):

(1) Where a company is a party to arrangements falling within section 47, Chapter 2 of Part 4 of FA 1996 (loan relationships) has effect in relation to the arrangements as if—

(a) the arrangements were a loan relationship to which the company is a party,

(b) any amount which is the purchase price for the purposes of section 47(1)(b) were the amount of a loan made (as the case requires) to the company by, or by the company to, the other party to the arrangements, and

(c) alternative finance return payable to or by the company under the arrangements were interest payable under that loan relationship.

FA 1996 which governs loan relationships contains a very extensive and complex set of provisions which apply to companies engaging in the lending or borrowing of money and paying interest or other finance costs. Section 50 (1) is not saying that section 47 involves the making of a loan; instead it taxes the company as if a loan had been made and as if the alternative finance return (the profit or loss under the murabaha or tawarruq transaction) were interest.

The UK’s approach here is similar to that in Malaysia, where the tax treatment of “profit” on Islamic financing transactions is assimilated to the tax treatment of “interest.”

Tax legislation in the UK has grown steadily since income tax became a permanent feature of the tax system in 1842, and was of course developed long before Islamic finance was contemplated in the UK. Not surprisingly, it happened to contain specific provisions which would impact upon Islamic transactions, even though the equivalent conventional transaction was not affected. These were addressed by specific legislation.

For example, the UK has long had a provision to counter companies disguising equity finance in the form of debt, in order to obtain tax relief for payments that are economically equivalent to dividends to risk bearing shareholders. This can be found in ICTA 1988 s.209 (2) (e) (iii):

(2) In the Corporation Tax Acts “distribution”, in relation to any company, means …(e) any interest or other distribution out of assets of the company in respect of securities of the company (except so much, if any, of any such distribution as represents the principal thereby secured and except so much of any distribution as falls within paragraph (d) above), where the securities are …(iii) securities under which the consideration given by the company for the use of the principal secured is to any extent dependent on the results of the company’s business or any part of it.

This provision would preclude Islamic banks offering investment accounts to their customers, since the profit share paid to the customer would be treated as a distribution. This means that the payment would not be tax deductible for the bank.

This problem is addressed specifically by FA 2005 s.54 which effectively disapplies ICTA 1988 s.209 (2) (e) (iii):

Profit share return [defined in FA 2005 section 49 in a form that corresponds to profit share return on investment account deposits of Islamic banks] is not to be treated by virtue of section 209(2)(e)(iii) of ICTA as being a distribution for the purposes of the Corporation Tax Acts.

The diminishing musharaka transaction outlined above presents relatively few difficulties from the perspective of corporate or personal income tax. The Eventual Owner is paying rent to the bank, and the deductibility or otherwise of this rent in most countries will depend on whether the property is occupied for business purposes or for personal use.

The UK has however legislated specifically for such transactions, by setting out precise requirements in FA 2005 s47A for a transaction called “diminishing shared ownership.” If a transaction falls within these rules, the rent being paid is treated for tax purposes as if it were interest, both for the payer and for the receiving financial institution. This is particularly important if the financial institution is not UK resident, since the UK always charges withholding tax on rent paid to foreign persons, whereas interest paid to foreign persons often has a reduced or zero withholding rate due to the operation of double taxation treaties.

The legislation in FA s47A is very precise. The financial institution can share in any losses on the asset. If the bank couldn’t share in any losses on the asset, then this contract would probably fail to be Shariah compliant and nobody would ever use it. However, FA s47A states that the bank cannot participate in increases in the value of the asset. This could become a problem. While many diminishing musharaka contracts are based upon the original purchase price, there is also a move by some organisations to have a contract which allows the financial institution to participate in the growth of the asset. This may be regarded by them as being slightly better from a Shariah perspective. Unfortunately such a contract does not satisfy the UK tax rules as they currently stand.

The most important question with diminishing musharaka however is the taxation of the property ownership changes, as many countries have some form of real estate transfer tax. In the case of a conventional bank mortgage, there is normally only a single taxable real estate transfer, from the vendor to the purchaser buying with the aid of a mortgage. However, in diminishing musharaka, the vendor sells to the bank, and the bank then sells to the eventual purchaser. Are there two incidences of real estate transfer tax?

The distinction between substance and form discussed above is not relevant, and a double real estate transfer tax charge will apply, in the absence of specific relief, even if the country adopts a substance based approach to taxation. That is the case in the Netherlands for example. In most countries, the double real estate transfer tax charge can only be eliminated if there is specific legislation to that effect.

Malaysia has enacted specific legislation. Section 2(8) of the ITA seeks to ignore the underlying transaction so that tax neutrality can be achieved in Islamic funding transactions, by providing that:

“… any reference in this Act to the disposal of an asset or a lease shall exclude any disposal of an asset or lease by or to a person pursuant to a scheme of financing approved by the Central Bank or the Securities Commission or LOFSA [Labuan Offshore Financial Services Authority], as a scheme which is in accordance with the principles of Syariah where such disposal is strictly required for the purpose of complying with those principles but which will not be required in any other schemes of financing.”

The requirement for advance approval negates any uncertainty in the application of the provision.

Similarly, the UK legislated relief from multiple charges to its real estate transfer tax called Stamp Duty Land Tax (SDLT) in FA 2003 s71A. This relief from SDLT was originally only available where the person renting or buying the property was an individual. In Finance Act 2006, the relief was widened because it was recognised that Muslims not only wanted to use this approach for the acquisition of personal residential property but also to acquire property for their businesses in a Shariah-compliant way and such a business might well be conducted by a company.

The treatment of Islamic finance transactions in computing business income may or may not need specific legislation. Muslim majority countries may not need legislation, illustrated by Egypt, or may choose to legislate to put the tax treatment beyond doubt as in the case of Malaysia. In the case of Western countries, if the tax system looks primarily to the substance of a transaction as with the Netherlands or the USA, specific legislation may not be needed. Conversely, if the tax system looks primarily to the legal form as with the UK, then specific tax legislation will be needed to ensure that Islamic finance transactions receive the expected tax treatment.

With regard to transaction taxes such as real estate transfer taxes, Islamic finance transactions risk incurring multiple charges to such taxes, compared to conventional transactions which bear only a single charge, unless the country concerned enacts specific legislation to prevent such multiple charges.

Advertisement

Click image

Follow @Mohammed_Amin