Serious writing for

serious readers

Summary

Posted 24 November 2010

The text below was written in November 2009 and finalised in early 2010 to form a chapter in the book "Islamic Investment Banking: Emerging Trends, Developments and Opportunities" edited by Sohail Jaffer and published by Euromoney Books.

My chapter is reproduced here with the consent of the publishers. My goal in writing it was to explain why the UK has been so sucessful as a centre for international Islamic finance.

At the time of writing, the UK is home to a number of Islamic financial institutions:

This number of Islamic financial institutions probably exceeds the total for the rest of Europe combined. International Financial Services London (IFSL) produces a report each year assessing the size of the global Islamic finance industry. Its report “Islamic Finance 2010” published in January 2010 stated a UK total of $19.4 billion in Shariah compliant financial assets, placing the UK eighth in the world, ahead of major Muslim majority countries like Pakistan, Turkey and Indonesia.

There are some landmark transactions in the public domain such as the acquisition of the Aston Martin car company by Investment Dar of Kuwait, and Qatari financing for the Shard of Glass (to be the tallest building in Europe) and the redevelopment of Chelsea Barracks.

As well as the relatively small dedicated Islamic banks in London, a significant role is played by the Islamic finance desks of conventional investment banks. These conventional investment banks are active as counterparties to Islamic banks in the UK and elsewhere, both in the interbank commodity murabaha market and in structuring more sophisticated investments. They have played specific roles in structuring and placing most of the jumbo sukuk issues to emerge from the GCC and South East Asia.

With their smaller balance sheets, the UK’s dedicated Islamic banks have focussed on smaller transactions that can be syndicated to their investor pools or accommodated on their balance sheets. They have also developed business which does not need significant use of their balance sheets such as private banking and asset management.

The UK has achieved this with a domestic Muslim population of only 2.4 million, fewer than 4% of the UK population. This small population significantly limits the domestic market for Islamic finance. However, London’s Islamic banks have shown that conventional UK companies are willing to borrow under Islamic principles provided the finance is available at competitive prices.

This chapter explains why the UK has such a dominant position. As discussed below, the reasons fall into two broad categories.

Finally, the chapter considers the scope for increased competition from other financial centres.

The UK has a significant advantage against many jurisdictions which seek to compete with it arising from its political stability. For over 300 years, the UK has had a stable system of government conducted in a transparent democratic framework.

This matters for international investors who may wish to channel very large amounts of money through legal structures that may be in place for generations as in the case of family trusts. While there are other countries such as the United States or Switzerland that offer similar levels of political stability, many Western countries do not, and there is no Muslim majority country that can compete with the UK on this criterion.

English law has become the law of choice for international financial transactions, with the only close competitor being the law of the state of New York. The key competitive advantage here is the highly developed state of the law and its ability to cope with complex financial transactions.

The English courts are a particularly attractive forum for the settlement of disputes, and have a key advantage over US courts in that a successful litigant can be awarded costs. Even where the awarded costs do not cover the full costs incurred by the successful litigant, the position is far better than under the US legal system where each party bears its own costs.

In the context of Islamic finance, the approach of the English courts to Shariah law provides significant benefits to investment banks and their customers by ensuring contractual certainty. The leading case in this area is the Court of Appeal decision in Beximco Pharmaceuticals Ltd v Shamil Bank of Bahrain E.C2004 EWCA Civ19. The governing law clause of the contract concerned read “subject to the principles of the Glorious Sharia’a, this Agreement shall be governed by and construed in accordance with the laws of England.”

The bank’s customer was seeking to avoid its liabilities to the bank by contending that the transaction was not fully compliant with Shariah. The key point about the approach taken by the Court of Appeal (which at the risk of extreme over-simplification can be described as disregarding any reference to Shariah) was that it achieved contractual certainty. Parties who contract under English law are therefore in a much clearer position than parties governed by the law of a Muslim majority country where there is much greater exposure to the contract being set side or varied by the courts on Shariah grounds.

An example is the recent doubt cast on the BBA contract (Al-Bai Bithaman, used in asset financing and house purchase) in Malaysia, where a first instance court decided that the contract was invalid under Shariah, although that was reversed by the Malaysian Court of Appeal in April 2009.

With a standard corporation tax rate of 28%, the UK is not generally regarded as a low tax territory. However, it has a number of advantages as an investment banking location:

Accordingly, investment banks are able to locate their investment management divisions in London to take advantage of the professional skills available without risking adverse tax consequences for their clients.

As an international investment banking location, London has some significant geographical advantages. It is close to continental Europe, and midway between the other major financial centres of Tokyo and New York. Accordingly staff based here are able to transact with both of those locations during the working day.

For transactions with Muslim majority countries spread across North Africa, the Middle East, the central Asian republics, South Asia and South East Asia, London is much closer than New York and shares more of the working day.

In addition to these physical factors are the long-standing UK connections with many Muslim majority countries, dating back to the days of the British Empire and now maintained by the Commonwealth.

The greatest single attraction of London as an investment banking location is the availability of very large numbers of skilled personnel; not just investment bankers but also accountants, lawyers, actuaries, consulting engineers etc. This has led many foreign headquartered banks to locate their investment banking division in London; in turn this attracts to London aspirant investment bankers from all parts of the world.

Once many investment banks are located in London, it makes sense for new ones to establish in the same place for ease of trading, communications and deal negotiation as well as staff recruitment. This network effect is the key reason why London is the most attractive location for Islamic investment banks that aim to do business globally, as opposed to serving a single geographical market.

London also benefits from the high standing of the UK’s academic institutions. These have traditionally helped to develop conventional bankers, but now the UK boasts a number of institutions offering Islamic financial training at the highest levels.

The March 2009 release of “The Global Financial Centres Index” again ranked London number one in the world. Whilst the report is published by the City of London Corporation, who obviously have a strong interest in the ranking, the report which is available free from their website derives this ranking from a number of objective criteria and a global survey.

The government has consistently supported the development of Islamic finance at least since 2003. In that year, the first tax legislation to facilitate Islamic finance was passed. It eliminated the double stamp duty land tax (SDLT, the UK’s real estate transfer tax) charge on murabaha or diminishing musharaka mortgages, to achieve equal treatment with conventional mortgages which entail only a single charge to SDLT.

The government regularly cites two policy reasons for its support.

A successful approach to adapting the UK tax system for Islamic finance

The UK is a pioneer among Western countries in adapting its tax system to facilitate Islamic finance. Without these changes, Islamic banks would not be able to operate in the UK as they would face excessive tax uncertainty.

As mentioned above, the UK started adapting its tax law in FA 2003 when it legislated to abolish the double charge to SDLT arising on Shariah compliant mortgage transactions. However, the most fundamental changes were introduced in 2005, specifically to enable the operation of Islamic banks in the UK.

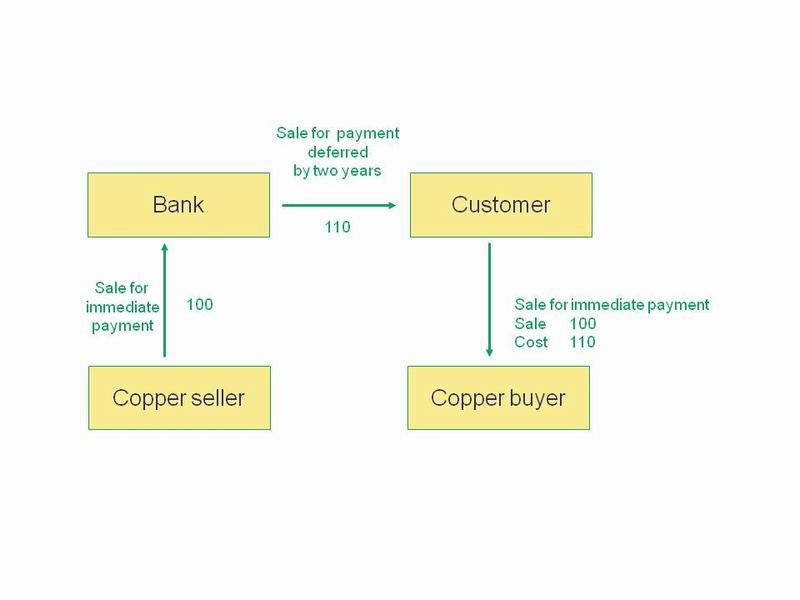

The reason why tax law changes were needed is most easily understood by considering the following commodity murabaha (purchase and resale) transaction. The purpose of this transaction is to allow the Bank to provide 100 of finance to the Customer, for two years, to earn a finance charge, in economic terms, of 10.

Diagram of a commodity murabaha transaction

Under UK tax law prior to the reform, the customer was probably not entitled to a tax deduction. The customer has purchased an amount of copper at a price of £110 payable in two years time, and sold that copper for £100 with the price being payable immediately. Accordingly, the customer has suffered a loss of £10. It was not clear that this loss was tax deductible.

Unless Customer could argue under UK tax law that it was trading in copper, it would not be entitled to deduct the £10 loss against its other income. Furthermore, even if Customer was a company that regularly traded in copper, this transaction does not look like a normal trading transaction since Customer knew that it would suffer a £10 loss when it commenced the transaction.

Accordingly, under pre-reform UK tax law, Customer would probably not obtain tax relief for its £10 cost, even though in economic terms it is clearly a finance cost. Therefore legislation was needed to ensure that obtaining finance through commodity murabaha transactions qualified for tax relief.

The tax law changes were introduced by FA 2005, with subsequent expansion of the range of transactions covered in FA 2006 and FA 2007. A review of the legislation enables one to ‘reverse engineer’ the design considerations that underlie it, in particular the following:

Strictly speaking, the UK has not enacted any Islamic finance legislation. A search of FA 2005 will fail to find words such as Islamic, Shariah, murabaha or any other term used specifically in Islamic finance. The reason is that the tax treatment of a transaction cannot be allowed to depend upon whether it is Shariah compliant. As well as introducing significant uncertainty into the UK tax system, introducing Shariah considerations would create a situation where all taxpayers were not receiving identical tax treatment.

Instead, the UK identified certain types of transaction widely used in Islamic finance, and ensured that those types of transaction received appropriate tax treatment. This is illustrated by FA 2005 s 47 “Alternative finance arrangements: purchase and resale” reproduced below as originally enacted:

47 Alternative finance arrangements: alternative finance return

(1) Subject to subsection (3) and section 52, arrangements fall within this section if they are arrangements entered into between two persons under which—

(a) a person (“X”) purchases an asset and sells it, either immediately or in circumstances in which the conditions in subsection (2) are met, to the other person (“Y”),

(b) the amount payable by Y in respect of the sale (“the sale price”) is greater than the amount paid by X in respect of the purchase (“the purchase price”),

(c) all or part of the sale price is not required to be paid until a date later than that of the sale, and

(d) the difference between the sale price and the purchase price equates, in substance, to the return on an investment of money at interest.

(2) The conditions referred to in subsection (1)(a) are—

(a) that X is a financial institution, and

(b) that the asset referred to in that provision was purchased by X for the purpose of entering into arrangements falling within this section.

(3) Arrangements do not fall within this section unless at least one of the parties is a financial institution.

(4) For the purposes of this section “the effective return” is so much of the sale price as exceeds the purchase price.

(5) In this Chapter references to “alternative finance return” are to be read in accordance with subsections (6) and (7).

(6) If under arrangements falling within this section the whole of the sale price is paid on one day, that sale price is to be taken to include alternative finance return equal to the effective return.

(7) If under arrangements falling within this section the sale price is paid by instalments, each instalment is to be taken to include alternative finance return equal to the appropriate amount.

(8) The appropriate amount, in relation to any instalment, is an amount equal to the interest that would have been included in the instalment if—

(a) the effective return were the total interest payable on a loan by X to Y of an amount equal to the purchase price,

(b) the instalment were a part repayment of the principal with interest, and

(c) the loan were made on arm’s length terms and accounted for under generally accepted accounting practice.

Reading section 47 above, it is clear that it was designed to set out tax rules for murabaha transactions. However it nowhere uses those terms and nothing in section 47 limits its application to Islamic finance. If a transaction falls within section 47, the tax treatment follows automatically, regardless of whether the transaction is (or was intended to be) Shariah compliant.

The following table sets out the key concepts that have been created in UK tax law, and the Islamic finance structures that they correspond to.

UK tax law concepts corresponding to common Islamic finance arrangements

Tax law |

Islamic finance |

Purchase and resale FA 2005 s 47 |

Murabaha |

Deposit FA 2005 s 49 |

Mudaraba |

Profit share agency FA 2005 s 49A |

Wakala |

Diminishing shared ownership FA 2005 s 47A |

Diminishing musharaka |

Alternative finance investment bond FA 2005 s 48A |

Sukuk |

Commercial sales of goods often involve a credit period for the customer. It would unduly complicate UK tax law if every sale of goods with deferred payment required identification of the price that would have prevailed if no credit were given, and then giving separate tax treatment for the implied cost of the credit. Consider for example a food manufacturer selling hundreds of thousands of tins of food to retailers with 30 days credit allowed for the payment of each sales invoice.

FA 2005 s 47 limits its impact by requiring the involvement of a financial institution in subsection (3). This ensures that only transactions where finance is provided by or to a financial institution fall within the new rules. Accordingly, the food manufacturer and its customers should not be impacted by these new rules. (One drawback of this approach is that it is currently impossible for two non-financial companies to transact Islamic finance with each other and receive the tax treatment given by the new legislation.)

Financial institution is defined in FA 2005 s 46(2) and in particular includes all UK licensed banks and all banks licensed in the European Economic Area which have exercised their European Union “passporting rights” to establish in the UK, and their wholly owned subsidiaries.

FA 2005 s 47 demonstrates how complex it can be to legislate for an apparently straightforward transaction. Drafting the new legislation would have been very arduous if it was then necessary to legislate specifically for all the tax consequences flowing from the transaction structures used in Islamic finance.

The legislation avoids this burden by assimilating the tax consequences of Islamic finance transactions into the existing tax legislation. For example, where a company undertakes a murabaha transaction, the tax consequences are governed by FA 2005 s 50 (1):

Where a company is a party to arrangements falling within section 47, Chapter 2 of Part 4 of FA 1996 (loan relationships) has (1) effect in relation to the arrangements as if—

(a) the arrangements were a loan relationship to which the company is a party,

(b) any amount which is the purchase price for the purposes of section 47(1)(b) were the amount of a loan made (as the case requires) to the company by, or by the company to, the other party to the arrangements, and

(c) alternative finance return payable to or by the company under the arrangements were interest payable under that loan relationship.

FA 1996 which governs loan relationships contains a very extensive and complex set of provisions which apply to companies engaging in the lending or borrowing of money and paying interest or other finance costs. FA 2005 s 50 (1) is not saying that section 47 involves the making of a loan; instead it taxes the company as if a loan had been made and as if the alternative finance return (the profit or loss under the murabaha transaction) were interest.

Tax legislation in the UK has grown steadily since income tax became a permanent feature of the tax system in 1842, and was of course developed long before Islamic finance was contemplated in the UK. Not surprisingly, it happened to contain specific provisions which would impact upon Islamic transactions, even though the equivalent conventional transaction was not affected.

These were addressed by specific legislation.

For example, the UK has long had a provision in TA 1988 s.209 (2) (e) (iii) to counter companies disguising equity finance in the form of debt, in order to obtain tax relief for payments that are economically equivalent to dividends to risk bearing shareholders:

(2) In the Corporation Tax Acts “distribution”, in relation to any company, means …(e) any interest or other distribution out of assets of the company in respect of securities of the company (except so much, if any, of any such distribution as represents the principal thereby secured and except so much of any distribution as falls within paragraph (d) above), where the securities are …(iii) securities under which the consideration given by the company for the use of the principal secured is to any extent dependent on the results of the company’s business or any part of it.

This provision would preclude Islamic banks offering profit sharing investment accounts to their customers, since the profit share paid to the customer would be treated as a distribution. This means that the payment would not be tax deductible for the bank.

This problem is addressed specifically by FA 2005 s.54:

Profit share return [defined in FA 2005 section 49 in a form that corresponds to profit share return on investment account deposits of Islamic banks] is not to be treated by virtue of section 209(2)(e)(iii) of ICTA as being a distribution for the purposes of the Corporation Tax Acts.

Unlike many countries where governments restrict the availability of banking licences because they wish to control how the national economy develops, the UK will grant a banking license to every applicant company that can demonstrate the necessary levels of capital, skilled personnel satisfying the fit and proper persons test, corporate governance standards etc.

The Financial Services Authority has built up a small team of people who understand Islamic finance, and has a policy of “no obstacles, but no special favours”. Accordingly Islamic banks are governed by the same regulations as conventional banks. The approach applied is to evaluate risks by looking at the economic reality of the transaction. For example, commodity murabaha transactions are almost always structured to minimise the bank’s exposure to commodity price risk. Accordingly, from a risk perspective the key risk is counterparty credit risk, not commodity price risk and the regulators evaluate the bank’s capital requirements taking that into account.

London faces competition from two types of location.

As the Malaysian government has given support to Islamic finance for over 25 years, Kuala Lumpur has developed into a significant Islamic financial centre. However, its focus has been primarily on the Malaysian domestic market, rather than selling the services of Malaysian banks to structure third country transactions.

Within the GCC, Bahrain is the traditional centre of Islamic finance, albeit facing competition from places like Dubai and Qatar.

The GCC centres have access to significant amounts of capital from both state institutions and ultra high net worth individuals. However, they lack the physical scale and depth of personnel of a location like Kuala Lumpur, while London dwarfs all of them when it comes to numbers of skilled financial professionals.

While forecasting is inherently uncertain, it is likely that Kuala Lumpur and the GCC centres will continue to dominate transactions that are inherently local. However, as Islamic finance becomes increasingly global, the factors that have given London such a strong position in conventional finance should enable it to take a clear leading position in international Islamic finance.

Many conventional financial centres have expressed a desire to develop their Islamic finance business. For example, Singapore has issued tax legislation for Islamic finance and Hong Kong has also expressed interest in the subject. Closer to London, Dublin and Luxembourg have a focus on asset management, while France has introduced tax law for Islamic finance to enable Paris to challenge London’s leading position.

All such competition much be taken seriously. Dublin and Luxembourg have both become domiciles of choice for conventional investment funds and are likely to attain a similar status for Islamic investment funds. However, while Paris has the benefit of a much larger French domestic Muslim population than the UK, and significant conventional strengths, it is unlikely to be able to successfully challenge London in Islamic finance just as it has failed to take first place in conventional finance.

New York has so far paid little attention to Islamic finance. However, as the world’s other pre-eminent conventional financial centre, it would pose the greatest challenge to London if it were to develop a serious interest in Islamic finance.

The global financial crisis has had no real impact on the relative competitive strengths of the financial centres discussed above. Both London and New York have suffered some reputational damage, but at the same time have seen strong government action to prevent systemic failure and to restore confidence, which some overseas centres (for example in the GCC) have suffered from other difficulties such as falling real estate prices leading to troubled banks.

The UK has been able to build upon its leading role as a conventional financial centre to attract Islamic banks to set up here. Despite some other Western countries having a significant presence in international financial services, the UK has been able to leverage its conventional financial status into establishing a leading role in international Islamic finance due to supportive government policy and rapid action in changing its tax law.

However, to maintain this lead the UK will need to remain supportive to Islamic finance. As well as continued refinements to its tax legislation, the UK needs to create a sterling Islamic yield curve by issuing government backed paper at a range of maturities. This would significantly assist the liquidity management of Islamic financial institutions in the UK who will be required to hold a proportion of their balance sheet in highly rated liquid assets.

Follow @Mohammed_Amin