Serious writing for

serious readers

They receive a stake in the firm's "carried interest" enabling them to pay capital gains tax instead of income tax.

Summary

Posted 28 February 2021 Correction added 1 March 2021

A colleague within the UK Shareholders' Association ("UKSA")recently asked me to explain the tax treatment of carried interest.

Having done so, I decided it would make a good article for "The Private Investor" which is UKSA's house magazine. It was published in the December 2020 edition, and you can read it below.

While it is always a mistake to look for logic in tax law (to paraphrase Donald Trump, “Tax law is what it is”), there are some general principles seen most of the time. For example:

When you work as a private equity executive, you do the same white collar work as many of us: reading things, attending meetings, writing reports, making phone calls, writing emails etc.

So how do you manage to pay tax on much of what you earn at capital gains tax rates instead of income tax rates?

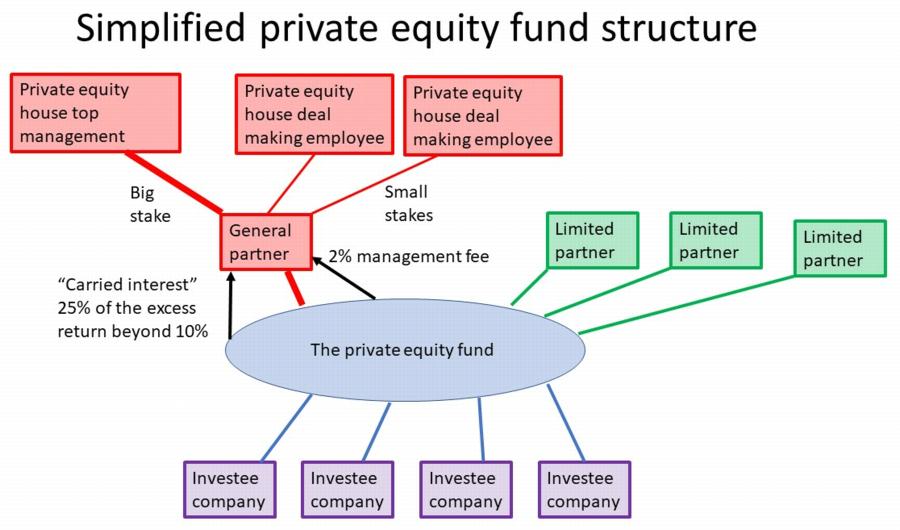

I have set out a simplified illustration below. In practice, private equity funds usually have very complex organisation charts. I have ignored that to make the principles easier to understand.

A private equity fund is normally structured as a limited partnership:

The general partner is typically entitled to make two charges to the fund:

The income from the annual management fee is used by the general partner to pay for the running costs of the private equity house. This includes the salaries of the employees who are the key deal makers. These salaries suffer regular income tax.

The key deal making employees normally also have fractional ownership stakes in the general partner company, either directly or indirectly.

When the fund is eventually closed out at the end of its life, assuming it has been successful, on the above numbers 25% of the excess return of the fund will be in the form of cash inside the general partner.

When the general partner is wound up, the key deal making employees will make gains on their shares since the general partner company is liquidated and the cash inside it is paid out.

The key question is what rate of tax should apply to the gain made on this liquidation.

There are many complicated rules in UK tax law applicable to shares which have some connection with your employment. These rules normally have the effect of taxing gains on such shares as ordinary income, where the top rate of income tax in the UK is 45% as stated above.

However, in the case of private equity and carried interest, UK tax law allows such gains to be taxed at the normal capital gains tax rate. [See correction at bottom of page.] That capital gains tax rate is currently 20% for higher rate taxpayers.

Accordingly, the continuation of this favourable tax treatment of carried interest, taxation at 20% [see correction] instead of 45% at top rates, is of great importance to the private equity industry in the UK.

Their threat is that if the UK eliminates this favourable tax treatment, they will emigrate, just as sports stars tend to emigrate once they become successful. Whether or not they are bluffing is a political question which I cannot answer.

Editor's note: Although Amin is a member of UKSA’s Policy Team, he is writing in a personal capacity. He is a retired PricewaterhouseCoopers tax partner.

When writing this article for UKSA, I simply checked the rates of capital gains tax published by HM Revenue & Customs on the GOV.UK website. In my professional work before retiring, I would never rely upon such a source but would always look at the source legislation.

A friend who is also a tax advisor pointed out that the rate I quoted appears wrong. It is indeed wrong; the correct rate of CGT on carried interest at present is 28%, which is still well under the top income tax rate of 45%.

The law is contained in TCGA 1992 s1H, of which I have reproduced just sub-sections (1)-(3) below. The key provision is (2)(b).

(1) This section makes provision about the rates at which capital gains tax is charged but has effect subject to—

(2) Chargeable gains accruing in a tax year to an individual that are—

are charged to capital gains tax at a rate of 18% or 28%.

(3) Other chargeable gains accruing in a tax year to an individual are charged to capital gains tax at a rate of 10% or 20%.

Follow @Mohammed_Amin