Serious writing for

serious readers

My article originally published in the magazine "Tax Notes International" looks at how South Africa, Singapore, Malaysia and the UK treat Islamic finance transactions for Value Added Tax (VAT) purposes. It also makes some general policy recommendations.

Summary

6 June 2016

Tax Notes International is an international tax magazine published both electronically and in hard copy by the non-profit organisation Tax Analysts. I recently wrote an article for them based on the VAT study that I have been undertaking in collaboration with the International Tax and Investment Center in Washington DC. It was published in the issue of 16 May 2016.

Now that the priority period I agreed to give the magazine has expired, I have reproduced my text below.

Mohammed Amin is a former U.K. head of Islamic finance and partner with PwC. He is based in London.

This article is an output from the research work on international tax aspects of Islamic finance transactions being conducted by the International Tax and Investment Center, with the financial support of the Qatar Financial Centre Authority.

In this article, the author discusses VAT issues regarding Islamic finance transactions and how some countries have addressed those challenges.

Most countries developed their tax systems in an environment of conventional finance. However, while Islamic finance transactions have similar economic objectives to conventional finance, they involve transactions that are usually very different. Accordingly, unless tax systems properly accommodate Islamic finance transactions, prohibitive tax costs can arise.

This applies to both direct taxes and indirect taxes such as value added tax, which some countries call goods and services tax. The article illustrates the VAT issues, using a hypothetical VAT rate of 20% throughout for simplicity.

Where all parties to a transaction are registered for VAT, and carrying on businesses which qualify for full recovery of VAT on costs, any VAT charges that arise represent no more than a short-term cash flow issue at worst. However, if a party is not in business (for example a retail consumer) or is conducting a business not able to recover VAT on all of its costs (for example a bank) then there is a risk of prohibitive VAT costs arising.

The article also looks at how some countries have dealt with these challenges and proposes a conceptual framework to assist VAT policy makers.

VAT is, by definition a tax on “value added”. When implemented it effectively operates as a form of consumption tax on final consumers.

In most cases tax authorities require businesses to compute VAT by totalling the VAT charged on all sales during the period (output tax), deducting the aggregate VAT paid on all purchases during the period (input tax), and paying the net amount to the tax authority. If the net amount is negative, the tax authority normally pays a cash refund to the business.

Conceptually finance costs are excluded when computing the value added of a business. Accordingly, the logic of value added tax requires that there be no VAT charged on interest payments. In VAT language, lending money at interest does not involve making a “taxable supply.” A consequence is that, in relation to their lending activities, banks cannot deduct input tax on their costs. Instead to them such input tax represents a cost.

For example, a $1,000 computer will cost a regular business just $1,000, as the $200 VAT also charged by the computer supplier is recoverable input tax. However, a $1,000 computer actually costs a bank $1,200 since the $200 VAT it has to pay to the computer supplier is not recoverable.

Governments sometimes deviate from the above simple treatment to encourage the location of certain types of banking activity within their jurisdiction.

For example, New Zealand allows banks to recover input VAT on the provision of financial services to a business 75% of whose supplies are taxable. Similarly, the UK enables banks operating in the UK which provide financial services to persons outside the European Union (EU) to recover VAT on overhead costs relating to the provision of those services.

While many different types of transactions take place in Islamic finance, this section uses just two relatively simple and very common ones to illustrate the difficulties that can arise.

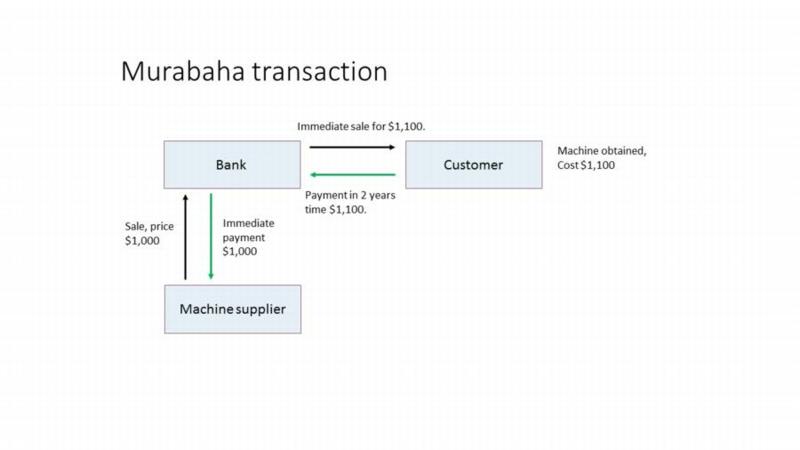

If the customer of a conventional bank requires finance to purchase a $1,000 machine, the conventional bank will lend $1,000 to the customer who then purchases the asset. In, say, two years’ time the customer will repay the $1,000 loan plus, say, $100 accumulated interest.

The analogous Islamic finance transaction is murabaha, where the bank will purchase the $1,000 machine, re-sell it to the customer at a higher price, here $1,100, with the mark-up being disclosed. The sale price is payable in two years’ time, in one lump sum. No interest is charged. This is illustrated below.

In the case of a conventional bank loan, there is a $1,000 taxable supply of the machine by the machine supplier to the customer with $200 VAT charged. If the customer carries on a business making taxable supplies, it can recover the $200 VAT, so the final cost of the machine to the customer is $1,000 plus $100 of interest, i.e. $1,100. (For simplicity, the customer’s cash flows relating to the $200 VAT payment and its recovery, if allowed, are ignored in both examples.)

In the case of the murabaha transaction, there are two supplies of the machine:

Often customers require finance from banks not for the purchase of specific assets but for other business purposes such as the payment of wages.

A conventional bank will simply lend money to the customer and charge interest. For example, $100 may be lent today at 5% simple interest, so $105 is repayable in 12 months’ time.

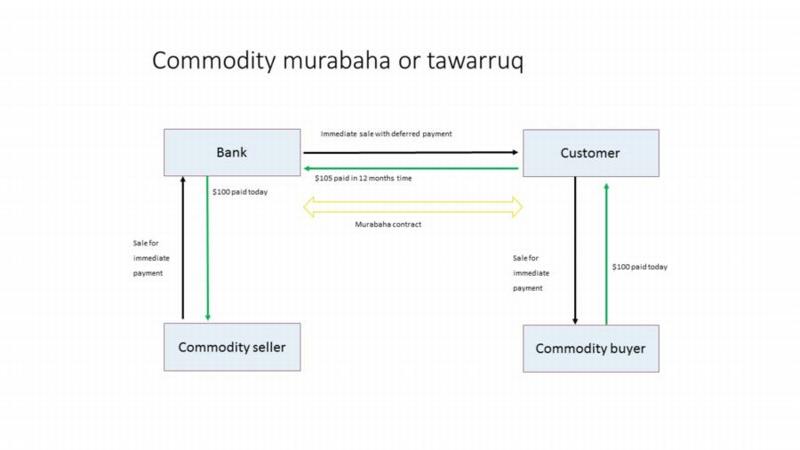

A common way for Islamic banks to provide cash to customers is a commodity murabaha transaction, also known as tawarruq.

The bank purchases a commodity, for example copper, for $100, making immediate payment. The bank then sells the copper to the customer, with immediate delivery but deferred payment, for $105. The $105 deferred price is payable in 12 months’ time. As soon as the customer owns the copper, it sells it for its open market value, $100 (ignoring any small bid/offer spread) for immediate delivery and immediate payment.

After the above transactions, the customer owns no copper but has $100 in cash. It is due to pay the bank $105 in 12 months’ time. Ignoring transaction costs, the economics for both the bank and the customer are identical to a $100 one-year loan at 5% simple interest.

There are three copper sales, each a supply of goods, subject to VAT in the absence of any special provisions.

Several countries with VAT systems have explicitly considered how Islamic finance transactions should be treated. The approach is relatively consistent

The South African VAT regime is set out in the Value-Added Tax Act, 1991 (Act No. 89 of 1991). Section 8A deals with Islamic finance.

For a murabaha transaction the client is deemed to have acquired the goods from the original seller, for the original sales price, and can recover (or not recover, depending on the client’s specific circumstances) VAT accordingly. The murabaha mark-up received by the bank is treated as an exempt supply of financial services.

In the murabaha example discussed earlier, the customer would be treated as purchasing the machine from the original seller for $1,000 (with $200 VAT), and would be in the same economic position as if it had taken out a conventional bank loan. No VAT would arise on the bank’s $100 mark-up under the murabaha transaction.

The definition of murabaha applied is contained in the Income Tax Act, 1962 (Act No. 58 of 1962) section 24JA.

The VAT law of Singapore is contained in the Goods and Services Tax Act, originally legislated in 1993 and revised in 2005.

The Fourth Schedule deals with Exempt Supplies, including financial services, and there are specific provisions within it for Islamic finance. For murabaha financing, paragraph 1(ra) treats the provision of the financing as an exempt financial service. The effective return earned by the bank is an exempt supply. Accordingly, in our example above the customer would not be faced with VAT being charged on the $100 mark-up earned by the bank, and the bank would charge only VAT of $200, equalising the Islamic finance and conventional finance transaction.

In Malaysia the Goods and Services Tax Act 2014 came into force relatively recently, 1 April 2015.

GSTA 2014 Schedule 2 is headed “Matters to be treated as neither a supply of goods nor a supply of services” and one of the categories, paragraph 5 is headed “Supply of goods or services under Islamic financial arrangement.”

It states:

5. Where any person makes a supply of goods or services under an Islamic financial arrangement, any supply made in such arrangement other than the provision of financing shall be treated as neither a supply of goods nor a supply of services.

The apparently straightforward consequence is that such supplies are ignored for GST purposes. However, the statute does not give details of exactly how it is to be ascertained which supplies are to be excluded from being supplies of goods or services.

Royal Malaysian Customs have issued a series of guides to the Goods and Services Tax, one of which has the title “Guide on Islamic Banking.” This goes through a number of Islamic finance transactions, itemising the supplies that take place, and explaining how the legislation quoted above is applied in practice.

The overall consequence is that in Malaysia the GST consequences to the customer, and the bank, from using Islamic financing should be the same as using conventional finance, since the intermediate supplies that take place within the Islamic finance transaction are ignored for GST purposes.

The legislation in South Africa, Singapore and Malaysia explicitly refers to Islamic finance transactions, with a relatively detailed definition. Strictly speaking, this introduces a religious test into secular tax law, which may not be acceptable to other countries.

As seen below, the UK takes a different approach. UK tax law proceeds by only looking at the economic implications of the transaction, without any concern for whether it qualifies religiously as Islamic finance or not, so religious tests do not enter into the UK tax system.

VAT is a harmonised tax within the EU. However, the EU has not specifically catered for Islamic finance in EU VAT law. Consequently, unlike the position with direct taxes, the UK cannot deviate from EU VAT by legislating for Islamic finance transactions.

However, HM Revenue & Customs (HMRC) has set out on its website its views on how UK VAT law applies to several common Islamic finance transactions.

The treatment of murabaha transactions is outlined in HMRC leaflet VATFIN8200 - Islamic products: Price plus "profit". It states:

“Where goods are sold with title to the asset passing from the bank to the customer the sale is treated in the same way as a credit sale (see paragraph 4.3 of Notice 701/49 Finance). There are two supplies being made by the bank – one of the goods and one of the facility to defer payment.

Consideration for supply of the goods will follow the normal liability rules. The “profit” element will be treated as consideration for the facility to defer payment and will be exempt under the VAT Act 1994, Schedule 9, Group 5, item 3.”

Consequently, the bank selling the machine above to the customer only charges the customer VAT on $1,000. This leaves the customer in the same VAT position as with a conventional loan.

To analyse the commodity murabaha transaction above, one needs to refer to another HMRC leaflet: “VAT Notice 701/9: commodities and terminal markets”.

As discussed in the general case above commodity murabaha becomes problematical if the customer is not engaged in a business which makes taxable supplies since significant VAT costs can arise.

The UK VAT regime for commodities and terminal markets, taken together with the UK’s special warehousing regime, significantly ameliorates, and in most cases eliminates, these potential problems.

While VAT Notice 701/9 covers many types of transaction, the one most likely to be encountered in Islamic finance is the sale of an identifiable commodity. For example, the subject of the commodity murabaha transaction may consist of copper where individually numbered bars of pure copper are bought and sold to achieve the desired economic consequences. Such transactions in copper would take place on the London Metal Exchange (LME), which is one of the terminal markets listed in VAT Notice 701/9 section 4.

As a result of this provision, in the commodity murabaha example, provided that the Commodity Seller and the Commodity Buyer are members of the LME, and provided the Bank and the Customer engage LME members to buy and sell the copper on their behalf, legally all of the transactions will be between LME members, either as principals or as agents with the copper never leaving the warehousing regime which allows sales of the copper to be treated as if they were taking place outside the UK. The result is that no VAT will be charged on any of the copper sales, leaving the customer in the same position as with a conventional bank loan.

The fact that the UK has not needed to legislate specifically for the VAT treatment of Islamic finance demonstrates that, by and large, the VAT regime applicable in the UK (and indeed throughout the EU) is capable of dealing with many Islamic finance transactions without giving rise to excessive VAT costs compared with the equivalent conventional finance transactions.

Consideration of the specific Islamic finance transactions mentioned above, and others excluded for space reasons suggests that they fall into some distinct categories, discussed below.

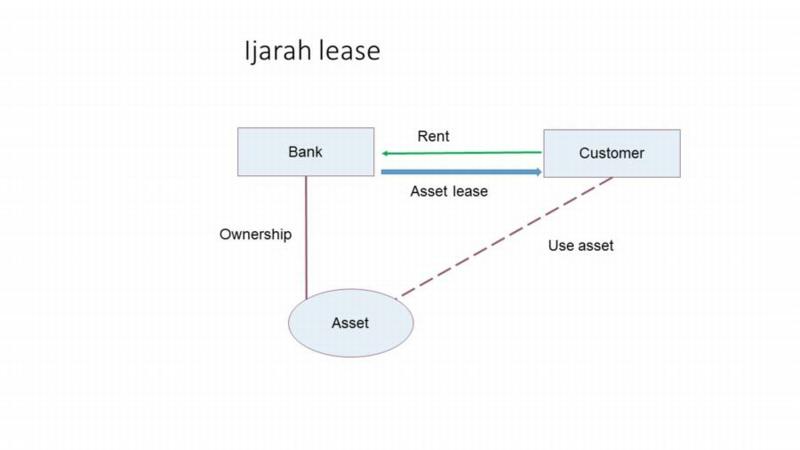

Some Islamic finance transactions involve almost identical transactions to their conventional counterparts. An example is ijarah (leasing which complies with some specific rules set by Shariah scholars) as in the diagram below.

The structure in the diagram does not look any different from a conventional asset lease.

Accordingly, an ijarah lease contract should not raise any significant VAT issues that are not raised by a conventional leasing contract.

The same will be true for other Islamic finance transactions which are structurally virtually identical to their conventional counterparts, in terms of the entities involved and their roles in the transaction and the cash flows.

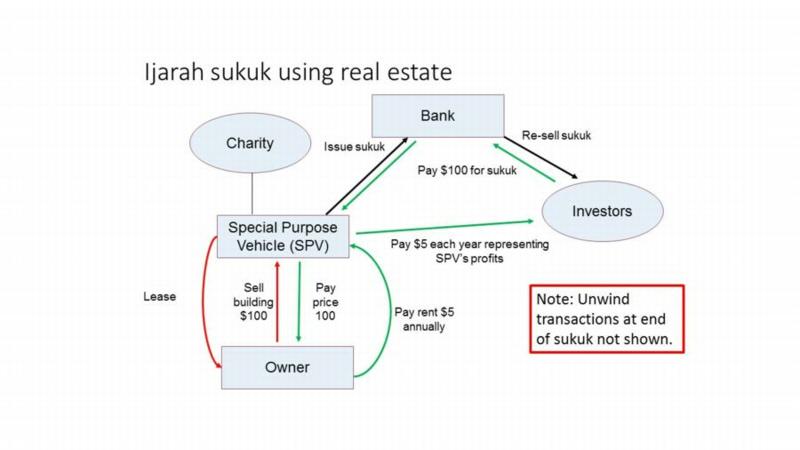

An Islamic finance transaction may have an “inner core” which is similar to a conventional finance transaction, but require many peripheral transactions to allow it to happen.

For example, multinational groups often issue interest paying bonds to investors from bond issuing SPVs which then lend the money borrowed to a group operating company. Similarly, sukuk (often colloquially called “Islamic bonds” even though they are not debt instruments) are issued by an SPV which passes the money raised to a group operating company.

However, as illustrated by the sukuk transaction below, a number of peripheral transactions involving a building are needed to enable the income stream on the sukuk to arise.

It may be the case that existing VAT law is adequate to allow these peripheral transactions to be carried out with adverse VAT costs in the form of irrecoverable VAT. Otherwise it will be necessary to bring in specific legislation to ensure these peripheral transactions do not cause additional VAT costs.

One example is the commodity murabaha or tawarruq transaction discussed earlier. This achieves the same economic outcome as a fixed term interest bearing loan, but the transactions are completely different from those of a loan.

Such transactions can involve multiple supplies of goods or services, which would not exist in the case of the equivalent conventional finance transaction. As illustrated above, this situation creates the greatest risk of the Islamic finance transaction giving rise to VAT costs, which would not arise in the case of the equivalent finance transaction. Unless existing tax law (such as the UK rules for commodities and terminal markets) already operates to avoid additional VAT costs, specific legislation will be needed to create parity of tax treatment between conventional finance and Islamic finance.

Follow @Mohammed_Amin