Serious writing for

serious readers

Summary

14 September 2012

The article below was originally published in the July-September 2012 issue of "New Horizon", the magazine of the Institute of Islamic Banking and Insurance.

At Islamic finance conferences, one is often asked whether Islamic financial institutions (IFIs) should account under International Financial Reporting Standards (IFRS) or under the accounting standards published by the Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI). This article discusses the following issues:

Given the breadth of the subject, the article concentrates on the high-level issues leaving readers to explore the details independently.

In most cases, there is no choice. Instead the accounting standards that an IFI must apply will be prescribed by the laws of the country in which it is incorporated or where it lists its securities.

For example European Union law requires all EU companies with publicly listed securities to prepare their consolidated accounts under IFRS. (More precisely, under IFRS subject to any modifications required by the EU.) Conversely the writer understands that all Bahraini and Qatari IFIs are required to account under AAOIFI.

The writer has not attempted a global survey. However a review of the accounts of Gulf Cooperation Council (GCC) IFIs showed that all GCC countries use IFRS apart from Bahrain and Qatar. IFRS is also the prevalent accounting standard almost everywhere except the USA which uses its own standards, albeit with the aim of converging with IFRS in the next few years. There are a few other countries such as Sudan which are understood to use AAOIFI.

The fundamental differences between IFRS and AAOIFI accounting standards arise from the different objectives of accounting, as seen by the two standard setting bodies.

IFRS are published by the International Accounting Standards Board (IASB). In 2001 the IASB adopted its "Framework for the Preparation and Presentation of Financial Statements." Paragraph 12 states:

"The objective of financial statements is to provide information about the financial position, performance and changes in financial position of an entity that is useful to a wide range of users in making economic decisions.”

In paragraph 33 and 34 the framework emphasises the need to faithfully represent the transactions that have taken place:

"To be reliable, information must represent faithfully the transactions and other events it either purports to represent or could reasonably be expected to represent. Thus, for example, a balance sheet should represent faithfully the transactions and other events that result in assets, liabilities and equity of the entity at the reporting date which meet the recognition criteria.

Most financial information is subject to some risk of being less than a faithful representation of that which it purports to portray. This is not due to bias, but rather to inherent difficulties either in identifying the transactions and other events to be measured or in devising and applying measurement and presentation techniques that can convey messages that correspond with those transactions and events. In certain cases, the measurement of the financial effects of items could be so uncertain that entities generally would not recognise them in the financial statements; for example, although most entities generate goodwill internally over time, it is usually difficult to identify or measure that goodwill reliably. In other cases, however, it may be relevant to recognise items and to disclose the risk of error surrounding their recognition and measurement."

Paragraph 35 emphasises the importance of substance over form:

"If information is to represent faithfully the transactions and other events that it purports to represent, it is necessary that they are accounted for and presented in accordance with their substance and economic reality and not merely their legal form. The substance of transactions or other events is not always consistent with that which is apparent from their legal or contrived form. For example, an entity may dispose of an asset to another party in such a way that the documentation purports to pass legal ownership to that party; nevertheless, agreements may exist that ensure that the entity continues to enjoy the future economic benefits embodied in the asset. In such circumstances, the reporting of a sale would not represent faithfully the transaction entered into (if indeed there was a transaction)."

AAOIFI was established in 1991 and published "Statement of Financial Accounting No. 1: Objectives of Financial Accounting for Islamic Banks and Financial Institutions" in 1993. The introduction to that statement says:

"Financial accounting in Islam should be focused on the fair reporting of the entity's financial position and results of its operations, in a manner that would reveal what is halal (permissible) and haram (forbidden).

Section 6/2 of the standard sets out the objectives of financial reports in six paragraphs of which the first is:

"Information about the Islamic bank’s compliance with the Islamic Shari’a and its objectives and to establish such compliance; and information establishing the separation of prohibited earnings and expenditures, if any, which occurred, and of the manner in which these were disposed of."

The above objectives can be summarised as follows:

Accordingly it should be no surprise if IFRS and AAOIFI standards give rise to different reporting when applied to the same transactions. Many examples can be found where IFRS and AAOIFI result in different accounting treatments for identical transactions, for example in the case of sale and leaseback illustrated in the Appendix.

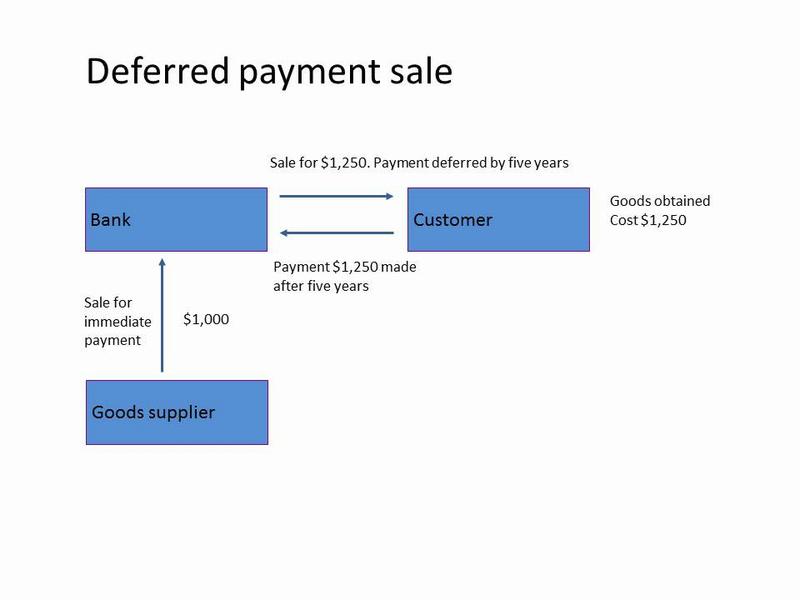

However even AAOIFI accounts often deviate from the legal form of the transaction in order to report the economic substance. Consider the deferred payment sale illustrated below:

Here the bank has bought a machine for $1,000 and resold the machine to its customer for $1,250 payable in five years’ time. It is clear that the $250 price uplift occurs only because the customer is allowed five years credit before making payment.

Paragraph 8 of AAOIFI Financial Accounting Standard No. 2 “Murabaha and Murabaha to the Purchase Orderer” requires the bank to defer the $250 profit on the sale. It states that the preferred method of accounting is “Proportionate allocation of profits over the period of the credit whereby each financial period shall carry its portion of the profits irrespective of whether or not cash is received.”

In simple terms the bank would recognise a profit of $50 in each of the five years, or perhaps it may be more sophisticated and spread the $250 over the five years using compound interest principles in which case it would recognise profits of $45.64, $47.72, $49.90, $52.18 and $54.56 in years 1 – 5 respectively computed as follows using the internal rate of return of 4.564%.

The profit allocation figures given above can be proved by the following table, using the internal rate of return of 4.564%.

Year |

B/f |

Profit |

C/f |

1 |

1,000.00 | 45.64 | 1,045.64 |

2 |

1,045.64 | 47.72 | 1,093.36 |

3 |

1,093.36 | 49.90 | 1,143.26 |

4 |

1,143.26 | 52.18 | 1,195.44 |

5 |

1,195.44 | 54.56 | 1,250.00 |

| 250.00 |

The legal and factual position is that the bank does everything needed to earn the profit on the day of the original transaction. Afterwards, it has a credit risk exposure for five years until the customer pays, but the bank needs to do nothing else other than wait five years for the $1,250 payment. The AAOIFI accounting recognises the economic reality that the bank’s $250 profit arises from giving the credit.

The principal drawback is that, because IFRS concentrates upon the economic substance rather than the legal form of the transactions, users of the IFI’s accounts may not receive sufficient information to form an informed view on whether the IFI’s transactions are Shariah compliant.

For example, the Appendix at the end of this page illustrates IFRS accounting for a sale and leaseback transaction where the asset remains throughout on the balance sheet of the original owner. This can make it harder to assess whether the sale and leaseback was conducted in a Shariah compliant manner.

However this risk can be mitigated by providing good quality additional disclosures. IFRS prescribes the basic accounting (for example requiring the sale and leaseback to be accounted for as a financing transaction), but IFRS does not prohibit the IFI from making additional informative disclosures in the notes to the financial statements. Accordingly the IFI can, and should, provide supplementary disclosures so that its shareholders and customers can satisfy themselves about the Shariah compliance of its transactions.

The starting point is to recognise that the apparent dichotomy between IFRS accounting and AAOIFI accounting is not real. With the exception of a few countries, most IFIs in the world account under IFRS.

Accordingly all of the emphasis should be on identifying the additional voluntary disclosures that should be made by IFIs accounting under IFRS. It would be very desirable to standardise these additional voluntary disclosures so that shareholders and customers of IFIs knew what additional disclosures to expect, and what constituted best practice.

Since AAOIFI brings together within one body both Shariah expertise and expert accounting knowledge regarding IFIs, it is well placed to devise the additional voluntary disclosures that IFIs accounting under IFRS should make. That would be a better use of AAOIFI’s resources than continuing to publish accounting standards that are applied in only a handful of countries.

Assume the following transactions:

IFRS is about reporting the economic substance of the transactions. From an economic perspective, the bank has provided $100 to the customer, in exchange for the customer’s obligation to pay it $5 on 31 December 2012 and 2013, and to pay it $115 on 31 December 2014.

Accordingly the bank does not record the building on its balance sheet, as it has no economic exposure to its value. Its economics are identical to the following loan transaction.

|

Loan B/F |

Interest |

Repayment |

Loan C/F |

2012 |

100.00 |

8.08 |

-5.00 |

103.08 |

2013 |

103.08 |

8.33 |

-5.00 |

106.41 |

2014 |

106.41 |

8.59 |

-5.00 |

110.00 |

Accordingly the bank would account as follows:

Income statement |

2012 |

2013 |

2014 |

Financial income from leasing |

8.08 |

8.33 |

8.59 |

Balance sheet |

2012 |

2013 |

2014 |

Investment in finance lease |

103.80 |

106.41 |

0 |

It appears appropriate under AAOIFI to account for the transaction that is actually taking place, which is a sale of the building and its eventual repurchase. The bank will show the building it purchases on its balance sheet, and report the rental income and the gain from selling the building in the periods when they arise.

This leads to the following accounting for the bank:

Income statement |

2012 |

2013 |

2014 |

Rental income from building |

5.00 |

5.00 |

5.00 |

Gain on sale of building |

|

|

10.00 |

Balance sheet |

2012 |

2013 |

2014 |

Building (cost) |

100.00 |

100.00 |

0.00 |

The total profit the bank makes is $25, regardless of whether accounting under IFRS or AAOIFI. However the periods in which it is reported are different. Also different is the balance sheet presentation.

Follow @Mohammed_Amin